How to Avoid the 7 Biggest Legal Mistakes When Starting a Business

You have the vision, the drive, and the groundbreaking idea. But a nagging fear lingers in the background: what if a hidden legal landmine derails your dream before it even takes off? For many Indian entrepreneurs, the world of compliance, registrations, and contracts feels like an intimidating maze of red tape. The fear of an unknown, costly error or the high price of legal advice can be paralyzing, keeping your focus away from innovation and growth.

This is where you gain clarity. Understanding how to avoid legal mistakes when starting a business is the single most important step in building a secure foundation. Forget the guesswork and overwhelming jargon. This guide provides a crystal-clear roadmap to navigate the seven biggest legal pitfalls for startups in India. You’ll get an actionable checklist that ensures peace of mind, prevents future disputes, and gives you the freedom to focus on what truly matters: turning your venture into a thriving success.

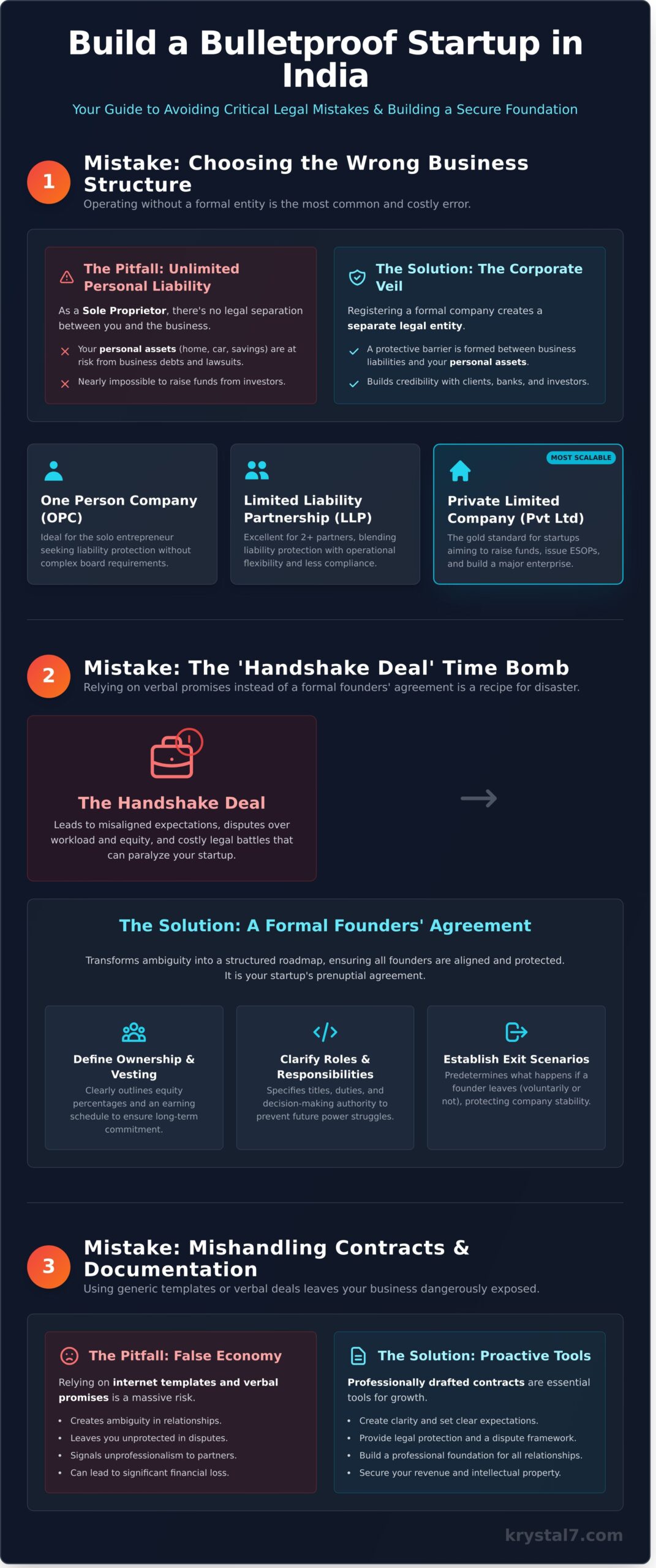

Mistake #1: Choosing the Wrong Business Structure (Or None at All)

One of the most common yet costly errors entrepreneurs make is starting operations without a formal legal structure. When you begin transacting as an individual, you are, by default, a Sole Proprietorship. This might seem like the simplest path, but it leaves you and your personal wealth completely exposed. The first step in how to avoid legal mistakes when starting a business is to build a strong legal foundation. A deliberate choice of business entity not only protects you but also prepares your venture for sustainable growth and future investment.

The Pitfall: The Danger of Personal Liability

As a sole proprietor, there is no legal distinction between you and your business. This is the world of ‘unlimited liability,’ meaning your personal assets are on the line. If a client sues your business or you accumulate debt, creditors can legally pursue your personal savings, car, and even your home. This structure also sends a clear signal to potential investors that the business is not formally organized, making it almost impossible to raise external funds.

Why It’s Critical: Setting the Stage for Growth

Formally registering your business as a Private Limited Company or LLP creates a ‘separate legal entity.’ This powerful legal concept establishes what is known as the ‘corporate veil’-a protective barrier between your business’s liabilities and your personal assets. This structure instantly builds credibility with clients, banks, and investors. It provides a clear framework for governance, ownership, and even for holding assets. For instance, a formal company can own its brand name and logo, a crucial first step in understanding intellectual property rights.

The Smart Solution: Assess Your Goals and Register Formally

Choosing the right entity is about aligning your legal structure with your business vision. Consider your number of founders, plans for fundraising, and capacity for statutory compliance. Here’s a simple guide for Indian startups:

- One Person Company (OPC): Perfect for the solo entrepreneur who wants limited liability without the complexity of a larger board.

- Limited Liability Partnership (LLP): An excellent choice for two or more partners, offering a blend of liability protection and operational flexibility with less compliance hassle than a Private Limited Company.

- Private Limited Company (Pvt Ltd): The most credible and scalable structure, ideal for startups planning to raise funds, issue employee stock options (ESOPs), and build a major enterprise.

This foundational decision shouldn’t be based on guesswork. Getting expert advice ensures your business starts on solid ground, giving you the freedom to focus on what truly matters: building your dream. Get clarity on the best structure for your vision.

Mistake #2: Neglecting a Formal Founders’ Agreement

In the exhilarating rush of launching a new venture, co-founders often operate on shared vision and mutual trust. This camaraderie is vital, but relying solely on verbal promises is a recipe for future disaster. The initial excitement can easily mask potential disagreements about roles, commitment, and the long-term direction of the company. A formal founders’ agreement is the single most important document you can create to protect your relationship and your business. Think of it as a prenuptial agreement for your startup.

The Pitfall: The ‘Handshake Deal’ Time Bomb

A simple handshake deal is a ticking time bomb. What starts as an equal partnership can quickly become unbalanced. Misaligned expectations on workload, financial contributions, and responsibilities breed resentment that can poison the company culture. Crucially, it leaves critical questions unanswered: What happens if a founder wants to exit? Do they walk away with their full equity stake, even if they leave after just a few months? Without a written agreement, these disputes can paralyze operations and lead to costly legal battles that your new venture cannot afford.

Why It’s Critical: Creating Alignment and a Clear Path Forward

A well-drafted founders’ agreement provides Krystal-Clear clarity from day one. It transforms ambiguity into a structured roadmap, ensuring all founders are aligned and protected. This is a fundamental step in how to avoid legal mistakes when starting a business. Its primary functions are to:

- Define Ownership and Vesting: It clearly outlines who owns what percentage of the company and establishes a vesting schedule. Vesting ensures that founders earn their equity over a set period, incentivizing long-term commitment.

- Clarify Roles and Responsibilities: It specifies each founder’s title, duties, and decision-making authority, preventing future power struggles.

- Establish Exit Scenarios: It pre-determines what happens in the event of a founder’s departure (voluntary or involuntary), disability, or death, protecting the company’s stability.

The Smart Solution: Document Everything Before You Launch

The solution is to formalise your partnership before you officially launch or seek funding. In India, this typically takes the form of a Shareholders’ Agreement for a Private Limited Company or a detailed LLP Agreement for a Limited Liability Partnership. While local regulations are paramount, foundational guides like the SBA’s 10 steps to start a business universally emphasize the importance of getting these structures right from the beginning. Your agreement should be comprehensive, covering equity splits, vesting clauses, intellectual property ownership, and dispute resolution mechanisms. Engaging a legal professional to facilitate these conversations and draft the document ensures it is robust, fair, and legally sound, giving you the freedom to focus on growth.

Mistake #3: Mishandling Contracts and Essential Documentation

Your business runs on a network of agreements-with clients, vendors, employees, and partners. Relying on verbal promises or generic templates downloaded from the internet is a false economy that can leave your venture dangerously exposed. Contracts are not just a defensive measure for when things go wrong; they are proactive tools that create clarity, set clear expectations, and build a professional foundation for every business relationship.

Poorly drafted or non-existent documents are a direct path to disputes over payments, the loss of valuable intellectual property, and unforeseen liabilities. Getting this right is fundamental to your operational stability and growth.

The Pitfall: The Risk of Vague or Missing Contracts

Without a clear, written contract, you are operating on memory and goodwill, both of which can fail under business pressure. This oversight often leads to critical issues. Unclear payment terms can delay revenue for weeks or even months, crippling your cash flow. Similarly, failing to precisely define a project’s scope is a classic recipe for ‘scope creep’-where clients demand extra work that was never budgeted for, leaving you to absorb the cost.

Why It’s Critical: Protecting Your Revenue and Operations

Well-defined legal documents are your first line of defense and a vital tool for success. In fact, mishandling agreements is one of the most common legal mistakes for startups, but it’s entirely preventable. A strong contractual framework provides:

- Revenue Protection: Iron-clad client contracts with clear payment schedules and late fee clauses ensure you get paid on time, every time.

- IP Security: Proper employment and contractor agreements clarify ownership of intellectual property and enforce confidentiality, protecting your most valuable assets.

- Liability Limitation: Robust Website Terms of Service and Privacy Policies are essential for limiting your legal exposure in the digital marketplace.

The Smart Solution: Create a Standard Set of Professional Contracts

A key strategy for how to avoid legal mistakes when starting a business is to build a library of legally sound documents tailored to your operations. Instead of scrambling for a contract when a deal is on the line, be prepared. Invest in professionally drafted templates for your core activities. Always get agreements in writing before any work begins or money changes hands. Crucially, ensure your contracts are specific to your industry and compliant with Indian law, as a generic template may not be enforceable in your jurisdiction.

Mistake #4: Ignoring Intellectual Property (IP) Protection

Many founders focus intensely on their product and operations, overlooking their most valuable long-term assets: their intellectual property. Your brand name, logo, proprietary software, and even your website’s content are intangible assets that define your market position and future value. Failing to protect them is not just a risk; it’s an open invitation for competitors to legally undermine your hard work.

The Pitfall: Losing Your Brand Before You’ve Built It

Imagine pouring your resources into building a brand, only to receive a legal notice forcing you to rebrand because your name infringes on an existing trademark. Or worse, a freelance developer you hired to build your app claims ownership of the source code. These are not hypothetical scenarios; they are costly, stressful realities that can derail a promising venture. Without clear legal ownership, your brand is built on unstable ground.

Why It’s Critical: Building a Defensible Business Asset

A key part of learning how to avoid legal mistakes when starting a business is treating your IP as a core asset, not an afterthought. Proper protection transforms your ideas into defensible, valuable property. A registered trademark grants you exclusive rights to your name and logo across India, preventing others from causing confusion in the marketplace. Copyright safeguards your creative works, while clear agreements ensure that any IP created for your company by contractors legally belongs to you, providing the clarity you need to grow securely.

The Smart Solution: Conduct Audits and Register Your IP

Proactive steps are essential to secure your intellectual property from day one. This isn’t complex red tape; it’s a strategic investment in your company’s future vision. A clear action plan provides the freedom to focus on growth.

- Perform a Thorough Search: Before you finalise your brand name and logo, conduct a comprehensive trademark search to ensure they are unique and available for use. This simple check prevents future conflicts.

- Register Early: File for trademark registration as soon as you are confident in your branding. In India, the “first to file” principle often prevails, and an early application provides priority rights.

- Clarify Ownership in Writing: Always use robust ‘work for hire’ or IP assignment clauses in your contracts with employees, freelancers, and agencies. This simple step explicitly transfers all intellectual property rights to your company, leaving no room for guesswork.

Don’t leave your most critical assets exposed. Protect your most valuable assets. Explore our Trademark Registration services.

Mistake #5: Confusing One-Time Registration with Ongoing Compliance

You’ve received your Certificate of Incorporation. The initial thrill is immense, but a crucial part of learning how to avoid legal mistakes when starting a business is recognizing that your legal obligations don’t end here. In reality, you’ve just crossed the starting line. Viewing incorporation as a one-time task instead of the beginning of a continuous compliance journey is one of the most common-and costly-missteps for new founders in India.

The Pitfall: The Silent Threat of Non-Compliance

The government requires businesses to prove they are active and compliant through a series of regular filings. Ignoring these statutory duties creates a cascade of problems that can quietly strangle a new venture before it has a chance to thrive. Key risks include:

- Heavy ROC Penalties: Missing deadlines for annual returns or financial statements with the Registrar of Companies (ROC) results in escalating daily penalties, which can quickly run into lakhs of rupees.

- Statutory Violations: Failing to maintain statutory registers, document board meetings, or adhere to the provisions of the Companies Act isn’t just poor governance; it’s a direct legal violation that can lead to director disqualification.

- Tax Scrutiny: Incorrect or late GST and TDS filings are major red flags for tax authorities, often triggering departmental audits, severe interest charges, and lasting damage to your business’s reputation.

Why It’s Critical: Maintaining Your ‘License to Operate’

Ongoing compliance is far more than just avoiding fines; it’s about maintaining your business’s very license to operate. A company in good legal standing is a company that can grow with confidence. A clean compliance record is non-negotiable when you approach banks for loans or investors for funding. They will always conduct thorough due diligence, and a history of non-compliance can instantly derail a promising deal, stopping your growth in its tracks.

The Smart Solution: Systematize or Outsource Your Annual Filings

The most effective way to manage this is to treat compliance as a critical business function and entrust it to experts. While you could create a compliance calendar, you’ll soon find that managing filings for ROC, Income Tax, and GST is a specialized, recurring task that pulls your focus away from your core mission: building your vision. Partnering with a professional firm removes the guesswork, eliminates the hassle, and ensures every deadline is met with precision. This gives you the clarity and confidence to lead your venture forward.

Gain the freedom to focus on growth. Discover our Annual Compliance Packages.

From Vision to Venture: Your Blueprint for Legal Success

Navigating the legal landscape of India is a critical first step in transforming your vision into a thriving enterprise. From choosing the right business structure to protecting your intellectual property and maintaining ongoing compliance, each decision builds the foundation for your future. Understanding how to avoid legal mistakes when starting a business isn’t just about preventing problems-it’s about creating the freedom to focus on what you do best: innovation and growth.

You don’t have to manage this complexity alone. With Krystal7, you gain a dedicated partner. Our team of Chartered Accountants and legal strategists offers expert guidance, while your dedicated relationship manager ensures you always have support. We operate with Krystal-Clear Transparency, meaning no hidden costs-just a solid foundation for your success.

Your dream deserves a secure start. Start your business on a solid legal foundation. Get your free consultation with Krystal7 today.

Frequently Asked Questions

Do I need a lawyer to start a business, or can I use an online service?

For standard business structures like a Private Limited Company or LLP, a professional online service offers a streamlined and cost-effective solution. These platforms are designed to bring clarity to the registration process, handling all documentation and statutory filings efficiently. However, if your startup involves complex intellectual property or requires bespoke shareholder agreements, consulting a dedicated legal strategist is a wise investment for tailored advisory.

What is the absolute first legal document I should prepare for my startup?

If you have co-founders, the most critical first step is creating a Co-founder’s Agreement. This foundational document provides essential clarity on roles, equity distribution, responsibilities, decision-making authority, and exit scenarios. It aligns all partners from day one, preventing future disputes and ensuring your venture is built on a transparent and secure legal footing. It is the blueprint for your partnership’s success.

How much should I budget for legal and registration fees in the first year?

In India, you should budget approximately ₹7,000 to ₹15,000 for the initial registration of a Private Limited Company. This covers government fees and professional charges. Beyond this, it’s vital to plan for mandatory annual compliance, which can cost between ₹15,000 and ₹25,000. This includes services like ROC filings, bookkeeping, and tax returns. Budgeting for both provides financial clarity and ensures your business remains compliant.

What’s the difference between a trademark, copyright, and patent in simple terms?

Think of them as protecting different parts of your vision. A Trademark protects your brand identity, like your logo or business name. Copyright automatically protects original creative works, such as your website’s code, articles, or design. A Patent protects a unique invention or process, giving you the exclusive right to it. Understanding these distinctions is a key part of knowing how to avoid legal mistakes when starting a business and protecting your assets.

Can I pay my co-founder or early employees with equity instead of a salary?

Yes, offering equity is a powerful way to compensate your founding team when cash flow is limited. However, this must be structured formally through legal documents like a Shareholder’s Agreement or an Employee Stock Option Plan (ESOP). It is crucial to include a vesting schedule, which ensures equity is earned over time. This protects your company’s ownership and aligns the team towards long-term growth and commitment.

What happens if I mix my personal and business bank accounts?

Mixing funds erases the legal line between you and your company, a principle known as the “corporate veil.” This can make you personally liable for business debts and liabilities. It also creates significant accounting challenges, complicates tax filings, and makes it difficult to track your business’s financial health. Maintaining separate accounts from day one is a non-negotiable step for legal protection and clear financial management.