Bookkeeping for Startups in India: The Ultimate Guide (2026)

You’re building a groundbreaking product, pouring every ounce of energy into your vision. But then the financial jargon hits: GST returns, TDS filings, and ROC compliance. Suddenly, the fear of a costly mistake feels overwhelming, and managing finances starts stealing time from what you do best-innovating. This is a common challenge, but it doesn’t have to be your story. Gaining control over your numbers is the first step to building a resilient venture, and effective bookkeeping for startups in India is the key that unlocks that control, transforming financial chaos into crystal clarity.

This ultimate guide for 2026 from Krystal7 Consultants is designed to help you master your startup’s finances from day one. We’ll cut through the complexity with a practical, step-by-step process designed for founders, not accountants. By the end of this article, you will have a clear roadmap to set up a streamlined bookkeeping system, the confidence that your business is compliant with Indian laws, and investor-ready financial records that empower smart decisions and fuel your growth. It’s time to gain the freedom to focus on your vision.

Why Bookkeeping is Your Startup’s Secret Weapon (Not Just a Chore)

For ambitious founders, viewing bookkeeping as a mere compliance task is a critical missed opportunity. It’s not just about filing taxes; it’s the engine of strategic growth. In the competitive Indian startup ecosystem, poor financial management isn’t just a mistake-it’s often a fatal one, leading to cash flow crises and stalled progress. Professional bookkeeping for startups in India moves you from guesswork to data-driven leadership, providing the crystal clarity needed to manage your runway and build a foundation for sustainable success.

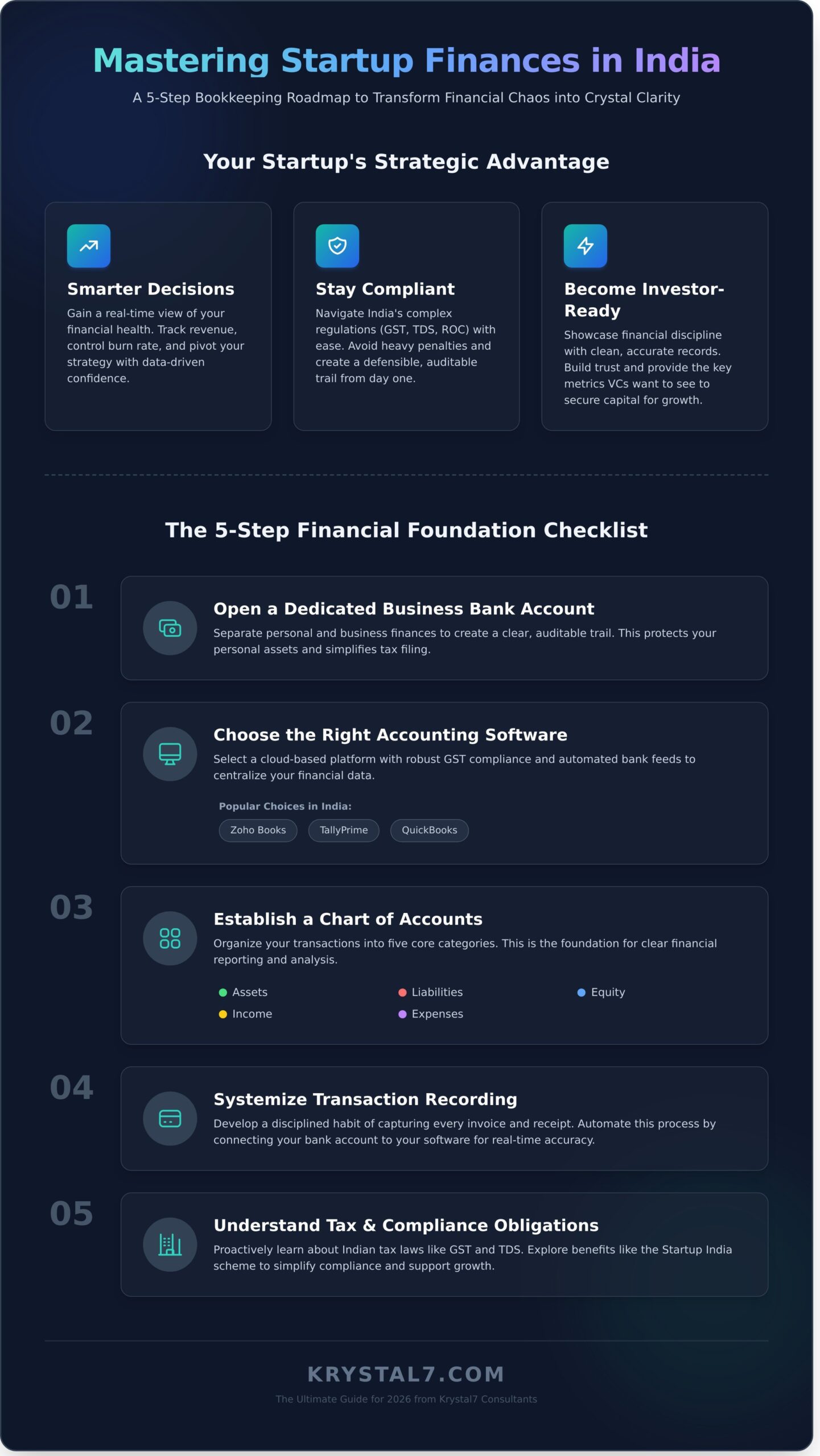

Make Smarter, Faster Business Decisions

Financial clarity, a core benefit of professional bookkeeping for startups in India, empowers swift, confident action. When your books are meticulously maintained, you gain an accurate, real-time view of your business’s health. This allows you to:

- Track revenue streams to identify your most profitable products or services and double down on what truly works.

- Analyse expenses to control your burn rate, spot inefficiencies, and optimize spending before it escalates.

- Pivot your strategy with precision, backed by hard data, not just a gut feeling about the market.

This transforms your financial records from a historical log into a forward-looking strategic tool.

Maintain Legal & Tax Compliance in India

Navigating India’s regulatory landscape can be a hassle, but it’s a challenge that expert bookkeeping for startups in India is built to handle. Non-compliance carries severe risks, with heavy penalties from the Ministry of Corporate Affairs (MCA), GST, and Income Tax departments that can cripple a young venture. Creating an auditable trail of every transaction from day one, following standard methods of bookkeeping, is your best defence against scrutiny. It ensures you are always prepared for timely filings of GST returns, TDS, and annual ROC forms, giving you the freedom to focus on growth, not red tape.

Become Investor-Ready from Day One

Investors don’t just back ideas; they back well-managed businesses. Proper bookkeeping for startups in India is a non-negotiable signal of your venture’s operational maturity. During due diligence, clean and accurate financial statements speak volumes, demonstrating that you are a disciplined and trustworthy founder. It enables you to:

- Showcase financial discipline and a clear understanding of your business’s health.

- Provide accurate financial data without last-minute scrambling or costly errors.

- Confidently track and report key metrics that VCs care about, like MRR, Burn Rate, and LTV.

This financial transparency builds the trust necessary to secure the capital your vision deserves.

Setting Up Your Financial Foundation: A 5-Step Startup Bookkeeping Checklist

Building a successful venture in India requires more than just a great idea; it demands a solid financial structure from day one. This practical checklist is designed to help you establish a robust system for bookkeeping for startups in India, creating clarity and control over your finances. Following these initial steps is crucial for avoiding the chaos that can derail a scaling business. By creating simple, repeatable processes now, you will save countless hours and prevent potential legal and compliance issues down the line.

Step 1: Open a Dedicated Business Bank Account

The first rule of professional finance is to never mix personal and business funds. A dedicated business bank account provides a clear, auditable trail of all your income and expenses. This separation is not just good practice-it’s essential for simplifying tax filing, proving your business’s legitimacy to investors, and protecting your personal assets. Choose a bank with a strong digital platform and features tailored for startups to streamline your operations.

Step 2: Choose the Right Accounting Software

Your accounting software is the central hub for your financial data. In India, popular and powerful choices include Zoho Books, TallyPrime, and QuickBooks. When selecting a platform, prioritize features that are critical for the Indian market: robust GST compliance, professional invoicing capabilities, and automated bank feeds. Cloud-based software is a game-changer, offering real-time access to your financials from anywhere, ensuring you can make informed decisions on the go.

Step 3: Establish a Chart of Accounts

Think of a Chart of Accounts as the index for your company’s financial story. It’s a structured list of every account used to record transactions, neatly organized into five core categories: Assets, Liabilities, Equity, Income, and Expenses. Most modern accounting software provides templates tailored for tech or service-based startups, giving you a strong starting point. A well-organized Chart of Accounts brings Krystal-Clear clarity to your financial reporting.

Step 4: Create a System for Recording Every Transaction

Financial accuracy depends on discipline. Develop a steadfast habit of capturing every invoice, receipt, and bill as it occurs. Leverage technology to make this process seamless-use mobile apps to scan and digitize physical receipts instantly. The most efficient step you can take is to connect your business bank account directly to your accounting software. This automates data entry, reduces human error, and gives you a real-time view of your cash flow.

Step 5: Understand Your Tax & Compliance Obligations

Proactive compliance is the key to hassle-free growth. From the outset, familiarize yourself with core Indian tax obligations like GST (Goods and Services Tax) and TDS (Tax Deducted at Source). Understanding these requirements early allows you to structure your finances correctly and explore benefits offered under government programs. For instance, the Startup India scheme provides valuable information on tax exemptions and simplified compliance measures designed to support new ventures.

Navigating Indian Compliance: GST, TDS, and ROC Explained for Founders

For many Indian startup founders, the world of statutory compliance can feel like a complex maze filled with acronyms. But navigating GST, TDS, and ROC filings doesn’t have to be a source of anxiety. Think of it as building a strong, legally sound foundation for your venture. A proactive approach, powered by meticulous bookkeeping, transforms these obligations from a hassle into a business asset, protecting you from penalties and building stakeholder trust.

This is where professional bookkeeping for startups in India provides crystal clarity, ensuring every transaction is correctly recorded and ready for reporting.

Goods and Services Tax (GST)

GST is a comprehensive indirect tax levied on the supply of goods and services. A startup must register for GST if its annual aggregate turnover exceeds ₹40 lakh for goods or ₹20 lakh for services (with lower thresholds for special category states). One of its key benefits is the Input Tax Credit (ITC), which allows you to claim back the GST you’ve paid on business purchases, reducing your final tax liability. To claim ITC accurately, your bookkeeping must be flawless, with every invoice properly recorded. This precision is essential for timely and accurate monthly or quarterly GST filings.

Tax Deducted at Source (TDS)

TDS is a mechanism to collect income tax at the very source of payment. As a startup, you are required to deduct a certain percentage of tax before making specific payments if they cross a defined threshold. This gives the government a steady revenue stream and tracks financial transactions. Common payments include:

- Salaries paid to employees

- Rent payments exceeding ₹2.4 lakh per year

- Payments for professional or technical services over ₹30,000

Your bookkeeping system must track these payments, ensure the correct TDS amount is deducted, deposited with the government on time, and reported through quarterly TDS returns.

Registrar of Companies (ROC) Filings

If your startup is a Private Limited Company or a Limited Liability Partnership (LLP), you have a mandatory annual reporting duty to the Registrar of Companies. These filings provide a transparent view of your company’s financial health and operational status. The two most critical forms are AOC-4 (for financial statements like the Balance Sheet and Profit & Loss Account) and MGT-7 (the Annual Return with details on shareholders and directors). The data for these crucial reports is pulled directly from your accounting records. Clean, organized, and up-to-date books make these annual filings a streamlined process rather than a year-end scramble.

Key Financial Reports: How to Read Your Startup’s Story in Numbers

Financial statements aren’t just for your Chartered Accountant; they are the founder’s most powerful strategic tools. They tell the story of your business-where you’ve been, where you are now, and where you’re headed. Learning to interpret these reports gives you the clarity to make smarter decisions and communicate your vision effectively to investors, partners, and your team. Proper bookkeeping for startups in India culminates in these three essential documents.

Let’s demystify the numbers and turn data into direction.

The Profit & Loss (P&L) Statement

The P&L, or Income Statement, answers the fundamental question: ‘Is my startup profitable?’ over a specific period, like a quarter or a financial year. It shows your financial performance by subtracting costs and expenses from revenues. By tracking your P&L, you can spot profitability trends, assess the impact of pricing changes, and identify opportunities to manage costs more efficiently.

- Revenue: The total income generated from sales of your product or service.

- Cost of Goods Sold (COGS): Direct costs tied to creating your product (e.g., raw materials, direct labour).

- Operating Expenses: Indirect costs to run the business (e.g., rent, salaries, marketing).

The Balance Sheet

Think of the Balance Sheet as a financial snapshot of your company at a single moment in time. It reveals what your company owns (Assets) and what it owes (Liabilities), providing a clear picture of your net worth (Equity). Investors scrutinise this report to assess your company’s financial stability and solvency. The entire report is built on one core equation: Assets = Liabilities + Equity.

The Cash Flow Statement

For an early-stage startup, cash is king. This report is arguably the most critical for survival as it tracks the actual movement of cash in and out of your business. It answers the crucial question: ‘Where did my cash go, and what is my runway?’ It breaks down cash activities into three areas-operating, investing, and financing-giving you a transparent view of your cash position and your ability to fund operations in the months ahead.

Mastering these reports provides the clarity you need to steer your venture confidently. This is how professional bookkeeping for startups in India transforms from a statutory hassle into a strategic advantage, giving you the freedom to focus on your vision. Need help turning your numbers into a clear story? Our experts are here to help.

DIY vs. Outsourcing: When to Hire a Professional Bookkeeping Service

As a founder, one of the most critical decisions you’ll face is how to manage your company’s finances. Choosing the right approach to bookkeeping for startups in India is a pivotal decision that directly impacts your ability to scale. Do you manage the books yourself to save on initial costs, or do you delegate to a professional to save time and ensure compliance? The answer depends entirely on your startup’s stage and vision for growth.

The Case for DIY Bookkeeping (Early Days)

In the pre-revenue or early bootstrapped phase, managing your own books can seem like the only logical choice. The primary advantages are the low initial cost, complete control over your financial data, and the deep understanding you gain of your company’s cash flow. However, the true cost isn’t just monetary; it’s the hours spent away from product development, sales, and strategy. This approach is also prone to errors that can become costly complications down the line.

The Power of Outsourcing to Experts

As your startup grows, outsourcing your bookkeeping transforms from a potential expense into a strategic investment. Partnering with a professional service saves you invaluable time, guarantees accuracy, and ensures you remain compliant with complex Indian regulations like GST and TDS. More importantly, it provides you with expert financial insights to make smarter business decisions. This is the clarity you need to build on. Get the Freedom to Focus on Growth with Krystal7 Consultants’ experts.

4 Signs It’s Time to Outsource Your Bookkeeping

If you’re on the fence, watch for these clear signals that your startup is ready for professional financial management:

- You’re spending more than 5 hours a month on bookkeeping. Your time is your most valuable asset. If financial admin is consuming time that should be spent on growth, it’s time to delegate.

- You’ve raised your first round of funding. Investors demand meticulous and accurate financial reporting. Professional bookkeeping ensures you maintain their confidence and meet all obligations.

- You’re preparing to hire your first employees. The complexities of payroll, Provident Fund (PF), and TDS deductions require expert handling to avoid compliance issues.

- You’re unsure about GST or TDS compliance. The penalties for non-compliance in India can be severe. If you’re losing sleep over tax deadlines, it’s a clear sign you need support.

Your Startup’s Financial Future: From Vision to Legacy

As we’ve explored, effective bookkeeping is far more than just tracking expenses; it’s the language of your business. From setting up a robust financial foundation to confidently navigating Indian compliance like GST and TDS, clean books provide the clarity you need to make strategic decisions and tell your startup’s growth story.

But you don’t have to navigate this complex landscape alone. The journey of mastering bookkeeping for startups in India can be overwhelming. Instead of getting lost in spreadsheets and statutory deadlines, you can gain a dedicated partner. At Krystal7, our team of Chartered Accountants and Company Secretaries provides all-in-one compliance and accounting packages, ensuring you have a dedicated advisor who understands your vision.

Stop the guesswork and gain the freedom to focus on what you do best-building your business.

Get Krystal-Clear Bookkeeping for Your Startup. Talk to an Expert Today!

Give your vision the financial clarity it deserves and build a legacy that lasts.

Frequently Asked Questions

What is the difference between accounting and bookkeeping for a startup?

Think of bookkeeping as the foundation. It is the meticulous day-to-day process of recording and categorising all your financial transactions, like sales, purchases, and payments. Accounting is the next level; it involves interpreting, analysing, and summarising this bookkeeping data to create financial reports. Bookkeeping gives you clean data, while accounting provides the strategic insights and clarity you need to guide your startup’s growth.

How much do bookkeeping services cost for a startup in India?

The cost for professional bookkeeping services in India for a startup typically ranges from ₹5,000 to ₹25,000 per month. The exact price depends on factors like your monthly transaction volume, the complexity of your business, and the scope of services required. Investing in expert services ensures compliance, provides financial clarity, and gives you the freedom to focus on your core business vision instead of administrative hassles.

Should my startup use cash basis or accrual basis accounting?

While the cash basis is simpler, recording transactions only when money changes hands, the accrual basis is mandatory for any startup registered as a Private Limited Company or LLP in India. Accrual accounting records revenue when earned and expenses when incurred, providing a far more accurate picture of your financial health. This method is essential for strategic planning, investor reporting, and meeting statutory compliance requirements.

What is the best accounting software for a small startup in India?

Several excellent options are tailored for the Indian market. Zoho Books is highly regarded for its strong GST compliance features and seamless integration within the Zoho ecosystem. TallyPrime remains an industry standard, widely used by Chartered Accountants across India, which can streamline collaboration. QuickBooks India is another popular choice, known for its intuitive, user-friendly interface that is great for founders new to accounting software.

How often should I reconcile my startup’s bank accounts?

Reconciling your bank accounts at least once a month is a critical financial discipline. This process ensures your records match the bank’s records, allowing you to catch any errors, fraudulent transactions, or missed payments promptly. For startups with high transaction volumes, a weekly reconciliation is even better. Consistent reconciliation is the key to maintaining an accurate cash flow picture and making informed financial decisions with confidence.

Can I do my own bookkeeping with no prior experience?

In the very beginning, with minimal transactions, it is possible to manage your own books using simple software. However, proper bookkeeping for startups India involves navigating GST, TDS, and other compliance norms where errors can be costly. As your business grows, partnering with a professional service is a strategic move. It eliminates guesswork, ensures accuracy, and frees up your valuable time to focus on scaling your venture.