Compliance for Private Limited Company: The Ultimate 2026 Checklist

You’ve transformed your vision into a registered Private Limited Company. The next step? Navigating the maze of statutory duties. If acronyms like ROC, MCA, and AOC-4 feel like a foreign language, and the fear of missing critical deadlines (and facing heavy penalties) is keeping you up at night, you are not alone. For many entrepreneurs, understanding the mandatory compliance for private limited company in India can feel overwhelming, pulling focus away from innovation and growth. It’s a common hurdle, but one you are about to clear with ease.

This is where the guesswork ends. We’ve created the ultimate 2025 compliance checklist to bring you absolute clarity. Forget the legal jargon and confusing timelines. This simple, step-by-step guide will walk you through every mandatory filing, from your first board meeting to annual returns, ensuring your business remains 100% compliant. It’s time to trade compliance anxiety for the confidence that comes from knowing your venture is legally secure, giving you the freedom to focus on what you do best: building your business legacy.

Why Compliance is a Strategic Advantage, Not Just a Legal Burden

For ambitious entrepreneurs in India, statutory regulations can often feel like a maze of red tape-a list of chores to be completed rather than a tool for growth. But this perspective misses the bigger picture. Proactive compliance for a private limited company is not a burden; it is the very foundation upon which a durable, scalable, and trustworthy business is built. Understanding what is compliance at its core reveals it’s a strategic framework that protects your vision, builds trust with stakeholders, and ensures your company maintains its active status, paving the way for long-term success.

The Benefits of a ‘Krystal-Clear’ Compliance Record

A meticulous record of compliance for a private limited company is one of your company’s most valuable assets. It moves beyond avoiding penalties and unlocks tangible business advantages that give you a competitive edge.

- Easier Access to Capital: Investors, venture capitalists, and banks conduct rigorous due diligence. A clean, transparent compliance record signals stability and low risk, making it significantly easier to secure funding and business loans.

- Enhanced Brand Reputation: In a crowded market, trust is everything. A fully compliant company demonstrates integrity and professionalism, building confidence with customers, suppliers, and potential partners.

- Protection from Liability: Properly managing the compliance for a private limited company protects directors from personal liability, hefty fines, and crippling legal disputes. It’s a shield that offers crucial peace of mind.

- Operational Agility: From day-to-day activities to major milestones like transferring shares or preparing for a merger, a flawless compliance record ensures every process is streamlined, smooth, and hassle-free.

Understanding the Key Authorities: MCA and ROC

Navigating the landscape of compliance for a private limited company means knowing the key players. In India, two bodies are central to this process. Think of them not as obstacles, but as the referees ensuring a fair and orderly business environment.

The Ministry of Corporate Affairs (MCA): This is the central governing body. The MCA sets the rules for all companies in India, administering the Companies Act and other corporate laws. It’s the ‘rulebook author’ for the entire country.

The Registrar of Companies (ROC): This is the local, state-level office of the MCA. Every state has an ROC responsible for the registration of companies and ensuring they file their required documents and returns. The ROC is the ‘local administrator’ who you interact with directly for all your filings.

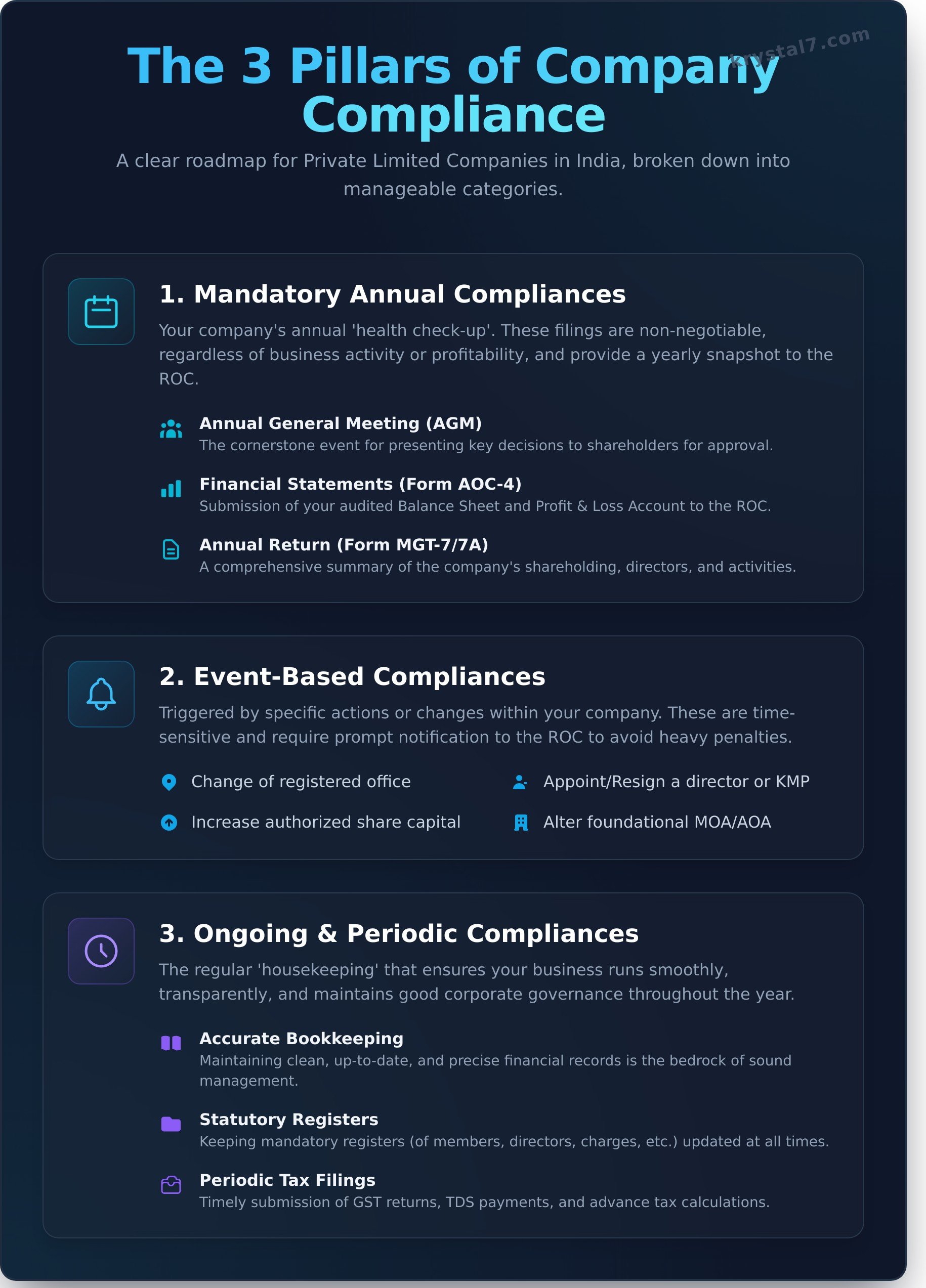

The Three Core Types of Compliance for Private Limited Company: A Simple Breakdown

Navigating the complex world of compliance for a private limited company can feel like trying to solve a puzzle with no picture on the box. The good news? It’s not a single, monolithic task. True compliance is an ongoing process, and we bring clarity by breaking it down into three simple, manageable categories. Thinking of it this way removes the guesswork and provides a clear, streamlined roadmap for your entrepreneurial journey.

1. Mandatory Annual Compliances

Think of these as your company’s mandatory annual health check-up. Regardless of whether your company made a profit, a loss, or had no activity at all, these filings are a non-negotiable part of the yearly compliance for private limited company. They provide a yearly snapshot of your company’s financial and structural health to the Registrar of Companies (ROC) and must be completed after the end of every financial year.

- Annual General Meeting (AGM): The cornerstone event where key decisions are presented to and approved by shareholders.

- Filing of Financial Statements (Form AOC-4): Submitting your audited Balance Sheet and Profit & Loss Account to the ROC.

- Filing of Annual Return (Form MGT-7/7A): A comprehensive summary of the company’s shareholding structure, directors, and corporate activities.

2. Event-Based Compliances

These compliances are triggered by specific actions or changes within your company. Just as you’d update your address with the bank after moving, your company must formally notify the ROC of significant events. These are highly time-sensitive, and missing the strict deadlines can lead to heavy penalties, making prompt and accurate filing a crucial part of the overall compliance for private limited company.

- Changing your company’s registered office address.

- Appointing, resigning, or removing a director or key managerial personnel.

- Increasing the authorized share capital or issuing new shares.

- Altering the company’s foundational documents (MOA/AOA).

3. Ongoing & Periodic Compliances

This category covers the regular “housekeeping” that ensures your business runs smoothly and transparently throughout the year. It’s about building a strong foundation of good governance from day one. This meticulous record-keeping is not just about avoiding regulatory hassle; it’s the bedrock of sound management and upholds the principles of corporate governance, building trust with investors, banks, and stakeholders.

- Accurate Bookkeeping: Maintaining clean and up-to-date financial records.

- Statutory Registers: Keeping mandatory registers (of members, directors, charges, etc.) updated.

- Periodic Tax Filings: Timely submission of GST returns, TDS payments, and advance tax calculations.

Your Mandatory Annual Compliance Calendar: Key Forms & Deadlines

Navigating the maze of statutory deadlines can be overwhelming. To bring Krystal-Clear clarity to your obligations, we’ve created a streamlined annual calendar. Think of this as your year-round reference guide, designed to eliminate guesswork and ensure your business remains in perfect standing. Mastering this timeline is the key to seamless compliance for a private limited company.

Post-Incorporation Compliance (The First 6 Months)

Once your company is born, the clock starts ticking on these foundational, one-time filings. Getting these right sets a strong precedent for future governance.

- First Board Meeting: Must be conducted within 30 days of incorporation to discuss key business matters and formalize initial operations.

- Appointment of First Auditor (Form ADT-1): Within 15 days of the first board meeting, you must appoint your company’s first statutory auditor and notify the Registrar of Companies (ROC).

- Commencement of Business (Form INC-20A): This is a crucial declaration, filed within 180 days of incorporation, confirming that the initial share capital has been received. You cannot begin business operations until this is filed.

Annual ROC Filings (The Core Calendar)

These filings form the core of your yearly compliance cycle. They provide the ROC with a transparent view of your company’s operational and financial health.

- Director’s KYC (Form DIR-3 KYC): All directors must verify their identity and address details annually by September 30th.

- Annual General Meeting (AGM): A mandatory meeting of shareholders that must be held within 6 months from the end of each financial year (i.e., by September 30th).

- Financial Statements (Form AOC-4): Your company’s audited financial statements (Balance Sheet, P&L Account) must be filed with the ROC within 30 days of the AGM.

- Annual Return (Form MGT-7/MGT-7A): This is a comprehensive summary of your company’s details, including its shareholding structure and directorships. It must be filed within 60 days of the AGM.

Other Important Annual Filings

Beyond the ROC, other statutory bodies also require regular updates to ensure complete compliance.

- Income Tax Return: For companies requiring a tax audit, the deadline to file the ITR is typically October 31st.

- MSME Returns (Form MSME-1): If your company has outstanding payments to Micro, Small, and Medium Enterprises, you must file this return twice a year.

- Return of Deposits (Form DPT-3): A mandatory annual filing by June 30th to disclose details of any outstanding loans or money received that is not considered a deposit.

Let our experts manage this complex calendar for you, giving you the freedom to focus on what truly matters: growing your vision.

Event-Based Compliances: When You Must Inform the ROC

Beyond your annual obligations, the journey of a growing business is marked by significant milestones and changes. Under the Companies Act, 2013, these are not just internal decisions; they are formal “events” that require you to notify the Registrar of Companies (ROC). Timely filing is a crucial aspect of compliance for a private limited company. Missing these deadlines doesn’t just attract heavy penalties; it can also render the business decision invalid, creating legal and operational hurdles down the line.

Think of it as keeping the official record of your company’s evolution accurate and transparent. To help you stay ahead, we’ve outlined the most common events that trigger a mandatory ROC filing.

Changes in Company Leadership

Your leadership team is the backbone of your company. Any change in its composition must be formally documented with the ROC to ensure legal validity. This provides clarity to all stakeholders, from banks to investors.

- Appointment or Resignation of a Director: Whether you are bringing a new visionary onto your board or accepting a director’s resignation, you must file Form DIR-12 within 30 days of the event.

- Changes in Key Managerial Personnel (KMP): The appointment or removal of a CEO, CFO, or Company Secretary also requires filing Form DIR-12 within the same 30-day timeline.

Changes in Company Structure & Address

As your venture grows, its foundational structure may need to adapt. These changes are fundamental to your company’s identity and must be reported without delay to maintain a clear statutory record.

- Change in Registered Office: Moving your official address? File Form INC-22 to notify the ROC. The timeline varies depending on whether the move is within the same city or to a different state.

- Increase in Authorised Share Capital: To issue more shares and raise capital, you must first increase your authorised capital and file Form SH-7.

- Allotment of New Shares: After receiving investment and issuing new shares, you must file a return of allotment using Form PAS-3 within 30 days.

Financial & Loan-Related Events

Significant financial activities, especially those involving loans and company assets, require ROC intimation to ensure transparency and protect the interests of lenders and shareholders.

- Creation or Modification of Charges: When you take a loan and offer company assets as security, a ‘charge’ is created. This must be registered with the ROC using Form CHG-1 within 30 days.

- Loans from Directors or Shareholders: Accepting unsecured loans from directors requires specific resolutions and declarations to ensure it complies with the Companies Act.

The rules can be nuanced, and knowing what constitutes a reportable ‘event’ is key to avoiding unnecessary red tape. Not sure if your decision needs a filing? Ask our experts for clarity.

The Real Cost of Non-Compliance: Penalties, Risks & Consequences

For ambitious entrepreneurs, compliance can sometimes feel like a background task. However, viewing it as optional is one of the most significant risks a business can take. The consequences of non-compliance extend far beyond a simple notice from the Registrar of Companies (ROC). Think of this not as a warning, but as a strategic map to protect the vision you’re working so hard to build. Understanding these tangible risks is the first step toward creating a resilient and trustworthy enterprise.

Monetary Penalties: A Growing Burden

The most immediate impact of delayed filings is financial. The Ministry of Corporate Affairs (MCA) imposes a straightforward but punishing late fee for forms like AOC-4 (Financial Statements) and MGT-7 (Annual Return). This isn’t a one-time fine; it’s a daily drain on your resources.

- Daily Compounding Fines: The penalty is ₹100 per day, per form, from the due date until the filing is completed. With no upper limit, this can quickly escalate into lakhs of rupees.

- Personal Liability: These penalties are levied not just on the company, but also on the Directors and officers responsible. This means your personal finances are directly at risk for corporate oversights.

Director Disqualification & Company Status

Persistent non-compliance triggers severe administrative actions that can paralyse your business. If a company fails to file its financial statements or annual returns for three consecutive financial years, the consequences are drastic. Directors of the company can be disqualified for a period of five years, and the company’s name can be struck off the ROC. This leads to an immediate operational shutdown, including frozen bank accounts and the inability to legally conduct any business.

Loss of Credibility and Future Opportunities

Beyond legal penalties, a poor compliance record severely damages your company’s reputation and closes doors to growth. A robust history of compliance for a private limited company is a non-negotiable for most stakeholders. Investors see it as a reflection of management’s discipline, lenders require it for loan approvals, and it’s often a prerequisite for participating in government tenders. During a crucial due diligence process for fundraising or an acquisition, a spotty compliance history can derail the entire deal or significantly lower your company’s valuation.

Navigating these complexities is where expert guidance brings clarity and peace of mind. Ensure your venture remains secure and focused on growth by partnering with a team that understands the intricacies of corporate compliance. For Krystal-Clear support, explore our advisory services.

How to Streamline Your Compliance: Your Path to Peace of Mind

Navigating the labyrinth of statutory deadlines, ROC filings, and board meetings can feel daunting. As an entrepreneur, your focus should be on growth and innovation, not getting bogged down in administrative red tape. The good news is that managing your annual compliance for private limited company doesn’t have to be a source of stress. Achieving seamless compliance is possible when you choose the right approach for your venture.

The DIY Approach: Pros and Cons

The primary allure of managing compliance yourself is the perceived cost savings. However, this path is fraught with risk. A single missed deadline or incorrect filing can lead to hefty penalties, sometimes running into lakhs of rupees. It’s a time-consuming process that demands constant learning to stay updated on ever-changing regulations. This approach is only truly viable for founders who already possess a deep background in corporate law or secretarial practice.

Hiring a Professional: The Strategic Investment

Engaging a professional firm is not an expense; it’s a strategic investment in your company’s stability and your own peace of mind. You gain immediate access to expert knowledge, ensuring every filing is accurate and on time. This proactive approach helps you avoid costly penalties and legal complications, freeing up your valuable time and mental energy to drive your business forward. It transforms compliance from a liability into a well-managed function of your business.

The Krystal7 All-in-One Compliance Package

At Krystal7, we believe your energy should be invested in your vision, not paperwork. We’ve designed our compliance package to give you exactly that-the Freedom to Focus. When you partner with us, you get more than a service; you get a dedicated compliance partner who brings crystal clarity to every requirement.

- A Dedicated Expert: You’re assigned a professional who understands your business and is always just a call away for guidance.

- Proactive Management: We track every deadline and handle all your filings proactively, so you never have to worry about missing a crucial date.

- Transparent Pricing: Our annual package comes with one Krystal-Clear fee. No hidden costs or surprise invoices. Ever.

Ready for hassle-free compliance? Explore our Annual Compliance Package today.

Secure Your Vision: Master Your Company Compliance with Confidence

Navigating the landscape of statutory requirements is not merely about avoiding penalties; it’s about building a resilient and reputable business foundation. As we’ve detailed, understanding your annual and event-based obligations is the first step. The second is transforming this legal necessity into a strategic advantage that fosters trust and stability. Managing the complexities of compliance for private limited company can feel overwhelming, but it doesn’t have to divert you from your core mission of innovation and growth.

This is where clarity meets action. Instead of wrestling with deadlines and red tape, imagine having the freedom to focus entirely on your vision, backed by unwavering expert support. Let our team of top-tier Chartered Accountants and Company Secretaries handle the details with Krystal-Clear Transparent Pricing. With a Dedicated Relationship Manager who knows your business, you gain more than a service; you gain a partner committed to your success.

Secure Your Business with Our All-in-One Annual Compliance Package.

Your business dream deserves an unshakeable foundation. Let’s build it together.

Frequently Asked Questions

What is the minimum compliance for a private limited company with no transactions?

Even with zero business activity, a private limited company must fulfill certain mandatory compliances. This includes appointing an auditor within 30 days of incorporation, holding a minimum of four board meetings annually, and maintaining statutory registers. Furthermore, you must file annual returns with the ROC (Form AOC-4 and MGT-7/7A) and a ‘NIL’ Income Tax Return to avoid penalties and maintain an active status. These steps ensure your company remains legally sound.

What happens if I miss the deadline for filing an annual return (MGT-7)?

Missing the filing deadline for forms like MGT-7 or AOC-4 results in significant penalties. The Companies Act imposes a daily penalty of ₹100 per form for each day of default, with no maximum limit. This amount can accumulate quickly, creating a substantial financial burden. Continuous non-compliance can also lead to the disqualification of directors and the company being marked as “struck off” by the Registrar of Companies (ROC), severely impacting its legal standing.

Do I need to appoint an auditor in the first year of my company?

Absolutely. Appointing a statutory auditor is a mandatory first step in your company’s compliance journey. The Board of Directors must appoint the first auditor within 30 days of incorporation. This appointment is then formalized by filing Form ADT-1 with the ROC. This is a non-negotiable requirement under the Companies Act, 2013, and a crucial foundation for the annual compliance for a private limited company, ensuring your financial statements are properly audited from day one.

How often do board meetings need to be held for a private limited company?

To ensure proper governance, a private limited company must hold its first board meeting within 30 days of incorporation. Following that, it is mandatory to conduct at least four board meetings every calendar year. A key rule to remember is that the gap between two consecutive meetings must not exceed 120 days. Maintaining proper minutes for each meeting is also a critical statutory requirement, providing a clear record of all board decisions and discussions.

Can I file all the ROC forms myself online?

While the Ministry of Corporate Affairs (MCA) portal is designed for online filing, it’s not a simple DIY process. Many crucial forms, including annual returns, require certification by a practicing professional such as a Company Secretary (CS) or a Chartered Accountant (CA). Attempting to file without expert oversight can lead to errors, rejections, and penalties. Partnering with a professional ensures accuracy, timeliness, and a hassle-free compliance experience, giving you the freedom to focus on your business.

What is the difference between a financial year and an assessment year?

This is a key concept for tax compliance. The Financial Year (FY) is the period from April 1st to March 31st, during which your company earns income. The Assessment Year (AY) is the year immediately following the FY, in which the income earned during that FY is evaluated and taxed by the authorities. For example, for income earned in FY 2024-25 (April 1, 2024 – March 31, 2025), the corresponding Assessment Year would be AY 2025-26.

What are statutory registers and do I need to maintain them?

Yes, maintaining statutory registers is a fundamental requirement of compliance for a private limited company. These are official, legally mandated records that contain vital company information, such as the Register of Members, Register of Directors, and Register of Charges. These registers must be meticulously maintained and kept at the company’s registered office. They serve as primary evidence of the company’s structure and are subject to inspection by authorities, making their accuracy paramount.

Article by

Nihal Srivastava

Nihal Srivastava is the Co-Founder of Krystal7 Consultants, helping Indian entrepreneurs and startups navigate company registration, compliance, trademark protection, and regulatory requirements with clarity and confidence. With 6+ years of hands-on expertise in MCA filings, GST compliance, and corporate structuring, Nihal has guided 1000+ businesses across India through their legal and compliance journeys. He believes every business dream deserves crystal clear foundations, and that no founder should be held back by paperwork or red tape.