Starting a New Company in India: A Founder’s 10-Step Guide

You have a brilliant idea, the drive to succeed, and a vision for the future. But turning that vision into a legally recognized new company can feel like navigating a complex maze of legal requirements and paperwork. For a first-time founder, this journey can be both exciting and overwhelming. The good news is, it doesn’t have to be. This guide provides a clear, step-by-step checklist, designed to transform your business idea into a fully compliant new company in India with confidence and clarity.

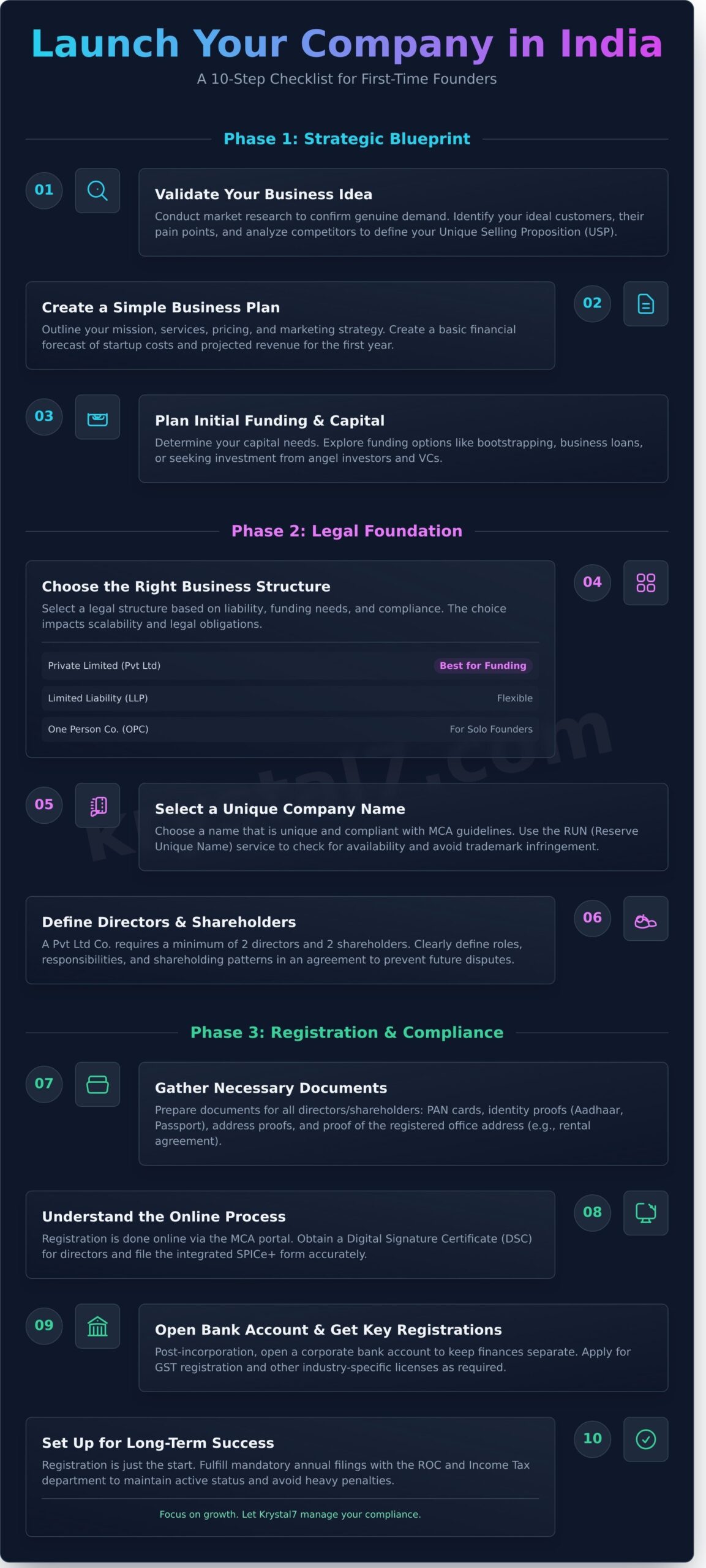

Phase 1: The Strategic Blueprint for Your New Company

Before you dive into any paperwork or legal filings, laying a solid strategic foundation is essential for long-term success. This initial phase is all about converting your raw idea into a viable and well-defined business concept. By focusing on validation, planning, and funding first, you set your new venture on the right path from day one.

Step 1: Validate Your Business Idea and Research Your Market

Every successful business starts by solving a real problem for a specific group of people. Before investing time and money, you must validate your idea. Ask critical questions: Who are your ideal customers? What specific pain point does your product or service address? Conduct thorough market research to understand your industry landscape, analyze your direct and indirect competitors, and identify what makes your offering unique-your Unique Selling Proposition (USP). Confirming that there is genuine demand for what you plan to offer is the most crucial first step.

Step 2: Create a Simple, Powerful Business Plan

A business plan doesn’t need to be a hundred-page document; it needs to be a clear roadmap. Start by outlining your company’s mission, vision, and core goals. Clearly describe your products or services, how you will price them, and your strategy for reaching customers. Most importantly, create a basic financial forecast. Estimate your startup costs (legal fees, software, marketing, etc.) and project your expected revenue for the first year. This simple plan will be your guide for making strategic decisions.

Step 3: Plan Your Initial Funding and Capital

With your business plan in hand, you can accurately determine how much capital you need to launch and operate until you become profitable. It’s time to explore your funding options. Will you be self-funding (bootstrapping) your venture? Or will you seek external capital through business loans, angel investors, or venture capitalists? Each path has significant pros and cons regarding control, equity, and pressure. Understanding these differences early will help you make the right financial choice for your new company.

Phase 2: Building the Legal Foundation for Your Business

With a solid strategy in place, you are ready to build the legal structure that will house your business. This is the phase where your company becomes a real, distinct entity in the eyes of the law. The decisions you make here regarding your business structure, name, and leadership will have a lasting impact and are crucial for preventing future complications.

Step 4: Choose the Right Business Structure in India

One of the most critical decisions a founder makes is choosing the right legal structure. The most common options in India are the Private Limited Company (Pvt Ltd), the Limited Liability Partnership (LLP), and the One Person Company (OPC). Consider factors like personal liability protection, ease of raising funds, ongoing compliance requirements, and your long-term scalability goals. A Private Limited Company is often the preferred choice for startups planning to raise investment and scale.

Step 5: Select a Unique and Compliant Company Name

Your company name is your identity, but it must also comply with the guidelines set by the Ministry of Corporate Affairs (MCA). The name must be unique and not too similar to existing companies or registered trademarks. You can check for name availability using the MCA’s RUN (Reserve Unique Name) service. It’s essential to avoid restricted words and ensure your chosen name does not infringe on any existing trademarks to prevent legal issues down the line.

Step 6: Define Your Directors and Shareholders

For a Private Limited Company in India, you need a minimum of two directors and two shareholders (they can be the same people). Directors are responsible for managing the company’s affairs, while shareholders are the owners. It is vital to clearly define the roles, responsibilities, and the shareholding pattern among the founders in a shareholders’ agreement to ensure alignment and prevent future disputes.

Phase 3: The Official Registration and Compliance Kick-off

You’ve planned, strategized, and made the foundational legal decisions. Now it’s time to make it official. This final phase covers the actual registration process with the government, from gathering documents to filing the necessary forms. Successfully completing these steps will set up your business for smooth financial and legal operations from the very beginning.

Step 7: Gather All Necessary Documents for Registration

To ensure a smooth registration process, gather all required documents beforehand. This typically includes:

- PAN cards for all directors and shareholders.

- Identity proofs, such as Aadhaar cards, Voter IDs, or passports.

- Address proofs for all directors.

- Proof of the registered office address (e.g., a rental agreement or utility bill).

Ensuring all documents are clear, valid, and up-to-date will prevent unnecessary delays in the application process.

Step 8: Understand the Online Company Registration Process

Company registration in India is now a streamlined online process handled through the MCA portal. The first step is obtaining a Digital Signature Certificate (DSC) for the proposed directors. The entire application is then filed using an integrated form called SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus). While the process is online, it is detailed and requires precision. This is where professional help can ensure every detail is handled accurately and efficiently, saving you time and preventing errors.

Step 9: Open a Corporate Bank Account and Get Key Registrations

Once your company is incorporated and you receive your Certificate of Incorporation, you must open a corporate bank account in the company’s name. It is mandatory to keep your business and personal finances separate. Depending on your business activity and turnover, you will also need to apply for GST (Goods and Services Tax) registration. You may also require other industry-specific licenses to operate legally.

Step 10: Set Up for Long-Term Success with Annual Compliance

Remember, company registration is just the beginning; ongoing compliance is a legal requirement for maintaining your company’s active status. All registered companies in India must adhere to mandatory annual filings with the Registrar of Companies (ROC) and the Income Tax department. Staying on top of these deadlines from year one is crucial to avoid heavy penalties and legal complications. Don’t get lost in paperwork when you should be focused on growth. Let Krystal7 manage your compliance.

Frequently Asked Questions

What is the fastest way to start a new company in India?

The fastest way is to use the online SPICe+ form with the help of a professional consultant. Having all your documents ready and your company name options pre-checked will significantly speed up the process, often reducing it to just a few working days.

How much does it cost to register a new company?

The cost includes government fees for registration and stamp duty, which varies by state, as well as professional fees for DSCs and consultation. Krystal7 offers all-inclusive packages with transparent pricing to avoid any surprises.

Can I register a company using my home address?

Yes, you can use your home address as the registered office address for your company, provided you have the necessary documents to prove your right to use the premises, such as a utility bill and a No Objection Certificate (NOC) from the property owner.

What is the difference between a Director and a Shareholder?

A Director is appointed to manage the day-to-day operations and strategic direction of the company. A Shareholder is an owner of the company who holds shares and has rights to a portion of the profits. In many startups, the founders are both directors and shareholders.

What happens if I miss a compliance filing deadline for my new company?

Missing a statutory deadline for annual filings results in significant financial penalties from the MCA, which increase daily. Continuous non-compliance can lead to the company being struck off the register and the directors being disqualified.

Starting a new company is a monumental step in an entrepreneur’s journey. By following this guide, you can navigate the process methodically and confidently, ensuring your business is built on a secure and compliant legal foundation. This clarity allows you to move past the paperwork and focus on what truly matters: growing your business and achieving your vision. Turn your dream into a registered company. Get started with Krystal7.

Article by

Nihal Srivastava

Nihal Srivastava is the Co-Founder of Krystal7 Consultants, helping Indian entrepreneurs and startups navigate company registration, compliance, trademark protection, and regulatory requirements with clarity and confidence. With 6+ years of hands-on expertise in MCA filings, GST compliance, and corporate structuring, Nihal has guided 1000+ businesses across India through their legal and compliance journeys. He believes every business dream deserves crystal clear foundations, and that no founder should be held back by paperwork or red tape.