FCTRS Filing in India: A Comprehensive Guide to RBI Compliance (2026)

What if a single administrative oversight on the RBI FIRMS portal could trigger a penalty reaching 100% of your transaction value? For many Indian entrepreneurs, the FCTRS filing process feels like a high-stakes obstacle course where one wrong step leads to a heavy Late Submission Fee (LSF). You’ve worked hard to secure foreign investment, and the last thing you need is a bureaucratic delay stalling your growth.

We know that the complex interface of the FIRMS portal and the strict FEMA pricing guidelines can feel incredibly daunting. It’s natural to worry about AD bank rejections or the steep penalties for missing the mandatory 60-day reporting window. You deserve a process that’s transparent and predictable so you can focus on your vision.

This guide will empower you to master the complexities of FC-TRS reporting and ensure your company remains in perfect standing with the RBI. We’ll break down the latest FEMA (Non-Debt Instruments) Rules 2019, explain the specific 2026 LSF calculation formula, and provide a clear roadmap for a successful filing that protects your operational liberty.

Key Takeaways

- Understand why Form FC-TRS is mandatory for capital instrument transfers between residents and non-residents to stay compliant with FEMA 1999 rules.

- Meet the strict 60-day reporting deadline to protect your company from significant Late Submission Fees (LSF) and regulatory scrutiny.

- Master the FCTRS filing steps on the RBI FIRMS portal, starting with the essential registration of Entity and Business User profiles.

- Apply Fair Market Value (FMV) pricing principles correctly to ensure your transaction meets the RBI’s mandatory floor price guidelines.

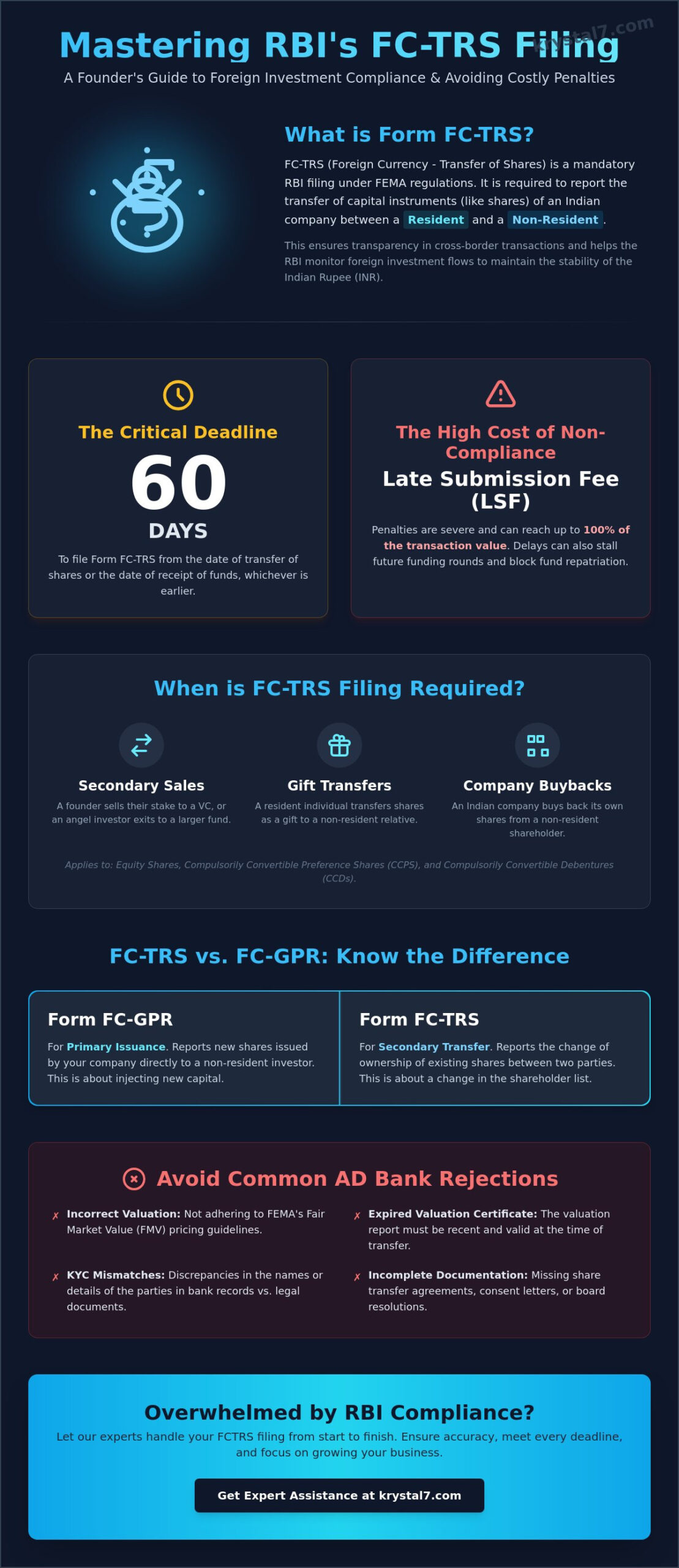

- Identify common reasons for AD bank rejections, such as expired valuation certificates or mismatched KYC data, to ensure a smooth approval process.

What is FCTRS Filing? Understanding the RBI Compliance Framework

Form FC-TRS stands for Foreign Currency – Transfer of Shares. It’s the primary mechanism the Reserve Bank of India (RBI) uses to track the secondary transfer of capital instruments. When a resident Indian sells shares of a Private Limited company to a non-resident, or vice versa, the transaction must be reported through the FCTRS filing process. This ensures that every shift in ownership across borders is documented with total transparency.

This compliance framework operates under the Foreign Exchange Management Act (FEMA), which governs all cross border financial activities in India. In recent years, the RBI has moved all reporting to the Foreign Investment Reporting and Management System (FIRMS) portal. This digital shift replaces older, paper-heavy methods with a streamlined, single-window interface designed to bring order to complex regulatory requirements.

The RBI monitors these transactions to maintain India’s balance of payments. By tracking the inflow and outflow of foreign currency, the government can manage the stability of the Indian Rupee (INR). For you as an entrepreneur, this filing isn’t just a checkbox. It’s a vital validation of your company’s valuation and legitimacy in the eyes of the regulator.

The Difference Between FC-GPR and FC-TRS

It’s easy to confuse different RBI forms, but their purposes are distinct. Form FC-GPR is used specifically for the primary issuance of fresh shares by an Indian company to a non-resident investor. In contrast, you’ll use Form FC-TRS for the secondary transfer of existing shares between parties. While FC-GPR reports new capital entry, FC-TRS tracks the change in ownership of existing capital.

Why Non-Compliance is a Risk to Your Business

Ignoring your FCTRS filing obligations creates a ripple effect of administrative and financial stress. During future funding rounds, sophisticated investors perform deep due diligence. Any missing filings or unresolved compliance issues can stall your investment or even kill the deal entirely. It sends a signal of poor governance that visionaries should avoid.

The financial impact is equally sharp. Late Submission Fees (LSF) act like compounding interest on your delay, growing larger the longer you wait to rectify the error. Beyond the costs, non-compliance can lead to restrictions on repatriating funds. You might find it impossible to send sale proceeds abroad or exit your business until the RBI grants a clean bill of health.

When is FC-TRS Reporting Required? Applicability and Deadlines

Identifying the exact moment you need to file Form FC-TRS is critical to avoiding heavy penalties. This requirement applies to the secondary transfer of capital instruments like equity shares, share warrants, and convertible instruments. Specifically, you must trigger an FCTRS filing when ownership shifts between a resident and a non-resident of India.

According to the RBI’s Master Direction on Reporting, the scope isn’t limited to just equity. It also covers Compulsorily Convertible Preference Shares (CCPS) and Compulsorily Convertible Debentures (CCDs). Even transfers between two non-residents require reporting if the Indian company is involved in the remittance process or if the transfer affects the company’s capitalization table.

Trigger Events for FCTRS Filing

Several common business scenarios demand immediate action. You must report the transaction if any of the following events occur:

- Secondary Sales: A founder selling their stake to a Venture Capital firm or an Angel investor exiting to a larger fund.

- Gift Transfers: When a resident individual transfers shares as a gift to a non-resident relative.

- Company Buybacks: When an Indian company buys back its own shares from a non-resident shareholder.

Each of these events changes the foreign investment profile of your business. If you’re unsure if your specific transaction qualifies, checking with a specialist at krystal7.com can clarify your obligations before you hit a deadline.

The 60-Day Countdown: Don’t Miss the Deadline

The RBI is incredibly strict about its timeline. You have exactly 60 days to complete the FCTRS filing. This countdown begins from the date of receipt or payment of funds, or the date of transfer of instruments, whichever happens earlier. This “whichever is earlier” clause is a common trap for entrepreneurs who focus only on the paperwork and ignore the cash flow dates.

For most Private Limited companies, the “date of transfer” is defined by the execution of the Share Transfer Form (SH-4). Don’t wait until the last week to gather your documents. Accurate reporting ensures that your annual compliance for private limited company remains intact and free from regulatory red flags. Missing this window doesn’t just lead to fees; it complicates your company’s legal standing for years to come.

FEMA Pricing Guidelines: Calculating Fair Value and Valuation

The Reserve Bank of India (RBI) maintains a watchful eye on how shares are priced during cross border transfers. This isn’t just about administrative record-keeping; it’s about ensuring that capital doesn’t move out of the country at an unfair rate. When you prepare your FCTRS filing, the valuation report serves as your primary evidence that the transaction is legitimate and follows the mandated FEMA pricing guidelines.

At the heart of these guidelines is the concept of Fair Market Value (FMV). For unlisted Indian companies, such as a Private Limited firm, the valuation must be determined using any internationally accepted pricing methodology. This calculation must be certified by a Chartered Accountant or a SEBI Registered Merchant Banker. Their expertise provides the transparency the RBI requires to approve the transfer of funds.

The Floor Price vs. The Cap Price

The RBI uses a firm logic to protect the Indian economy through two specific rules. If a resident Indian sells shares to a non-resident, the price cannot be lower than the Fair Market Value. This is known as the “Floor Price” rule, designed to prevent Indian assets from being sold too cheaply. It ensures that the country receives adequate foreign exchange for its equity.

Conversely, when a non-resident sells shares to a resident, the price cannot exceed the Fair Market Value. This “Cap Price” rule prevents an excessive outflow of the Indian Rupee (INR). Both scenarios rely on the “Arm’s Length” principle. This means the transaction price should reflect what two independent, unrelated parties would agree upon in an open and competitive market.

Documents Needed for Valuation Compliance

Obtaining a successful FCTRS filing approval requires a meticulous approach to documentation. Your Authorized Dealer (AD) bank will scrutinize your valuation report to ensure it aligns with the actual funds transferred. You should ensure your valuation certificate is recent, as stale reports are a frequent cause for bank rejection. Generally, the valuation should be conducted as close to the transaction date as possible to reflect the current health of the business.

Beyond the valuation certificate, you’ll need to provide several supporting documents to complete the compliance trail:

- Share Purchase Agreement (SPA): This document outlines the agreed-upon terms, price, and number of shares being transferred.

- Foreign Inward Remittance Certificate (FIRC): This acts as proof that the funds have entered the Indian banking system from an overseas account.

- KYC of the Non-Resident: The AD bank requires “Know Your Customer” documents to verify the identity and legitimacy of the foreign party involved.

Step-by-Step Process for FCTRS Filing on the RBI FIRMS Portal

The RBI FIRMS portal is the digital gateway for all foreign investment reporting in India. Navigating this interface requires a methodical approach to ensure your data matches your bank records perfectly. A successful FCTRS filing begins with setting up the correct user architecture before you even touch the reporting forms.

Establishing this foundation prevents technical delays that could push you past your 60-day deadline. The portal is designed for transparency; it requires specific roles to be defined for the Indian company and the person performing the submission.

Stage 1: User Registration and Entity Mapping

You must first register an “Entity User” profile. This is a one-time registration for the Indian company and requires an authority letter from the board of directors. Once the Entity User is active, you can then register a “Business User” profile. This is the account used by the professional or employee who will actually submit the reporting data.

The Business User registration isn’t instant. Your Authorized Dealer (AD) bank must review and approve this profile. This step ensures that only authorized representatives can submit sensitive financial data on behalf of your Private Limited company.

Stage 2: Form Submission and AD Bank Liaison

After your Business User profile is live, you can log in to access the FC-TRS form. The portal organizes the filing into logical tabs. You’ll need to provide precise details for both the transferor and transferee, including their PAN and residential status. Accuracy in your CIN and PAN is non-negotiable; any mismatch with MCA records will lead to an immediate rejection.

The “Capital Instruments” tab requires the specific number of shares and the face value. Meanwhile, the “Remittance” tab must align exactly with your Foreign Inward Remittance Certificate (FIRC). If you’ve missed the 60-day window, the portal includes a “Reason for Delay” field where you must explain the circumstances to the regulator. Once you submit, track your “Application Status” regularly to see if the bank has approved or rejected the entry.

To ensure your documents are formatted correctly and meet all technical portal requirements, you can consult with our compliance experts to avoid common filing errors.

Make sure you have these mandatory attachments ready for upload:

- Consent letters signed by both the buyer and the seller.

- The certified valuation report from a Chartered Accountant or Merchant Banker.

- The FIRC or proof of out-bound remittance.

- KYC documents for the non-resident party involved in the transfer.

Avoiding Rejections and Penalties: How Krystal7 Simplifies Compliance

The Authorized Dealer (AD) Bank acts as the first line of scrutiny for your FCTRS filing. They don’t just forward your documents to the RBI; they perform a meticulous audit of every detail. Even a minor mismatch between your Foreign Inward Remittance Certificate (FIRC) and the share transfer form can trigger a rejection loop. This back-and-forth isn’t just frustrating; it creates a cycle of administrative anxiety that visionaries should never have to endure.

If you miss the mandatory 60-day window, the RBI imposes a Late Submission Fee (LSF). Under current regulations, the LSF starts at ₹7,500 plus a percentage based on the transaction amount and the length of the delay. For more serious or prolonged delays, a simple LSF might not be enough. In these cases, you may need to undergo the “Compounding” process. This involves voluntarily admitting the contravention to the RBI to regularize the transaction and avoid future legal hurdles.

The Rejection Checklist: Audit Your Filing Before Submission

To ensure a smooth approval from your AD Bank, you must verify your documentation against their internal requirements. Use this checklist to catch errors before they lead to a rejection:

- FIRC Alignment: Verify that the amount mentioned in the FIRC matches the transaction value in your share purchase agreement exactly.

- Proper Stamping: Ensure the Share Transfer Form (SH-4) is properly stamped and signed by all parties involved.

- Data Consistency: Confirm that your private limited company india master data on the MCA portal is identical to the details you’ve entered on the FIRMS portal.

Krystal7’s Expert Compliance Management

At Krystal7, we believe in bringing visual clarity to the often-opaque world of regulatory compliance. Our transparency motif means you receive clear timelines and fixed fee structures with no hidden surprises. We understand that your time is your most valuable asset. Our liberation theme is centered on taking the weight of RBI paperwork off your shoulders so you can focus entirely on scaling your business.

We handle the end-to-end liaison with your AD Bank, resolving queries before they turn into rejections. Our team of professionals ensures that every FCTRS filing is methodical, accurate, and submitted well within the deadlines. Don’t let bureaucratic complexity stall your growth or lead to heavy penalties. Contact Krystal7 at business@krystal7.com or visit krystal7.com for a seamless, expert-led compliance experience today.

Securing Your Global Growth Through Compliance

Navigating the intricacies of RBI reporting doesn’t have to be a source of stress for your business. By mastering the 60-day reporting window and adhering to FEMA pricing guidelines, you protect your company from heavy penalties and ensure future funding rounds remain uninterrupted. A methodical FCTRS filing process is the best way to maintain total transparency with regulators while preserving your operational liberty.

Success on the FIRMS portal relies on accurate valuation certificates and precise data mapping that aligns with your AD Bank’s expectations. Our Gurgaon-based team of experts specializes in FEMA and RBI compliance, offering you a proven track record of 100% approval rates. We provide transparent pricing with no hidden bureaucratic costs, allowing you to delegate the paperwork and focus on your vision.

Don’t let RBI compliance slow down your growth. Contact Krystal7 Consultants at business@krystal7.com for expert FCTRS filing assistance. We’re here to be your trusted partner in every step of your entrepreneurial journey.

Frequently Asked Questions

What is the time limit for FCTRS filing with the RBI?

You must complete your FCTRS filing within 60 days from the date of the transfer of capital instruments or the receipt/remittance of funds, whichever happens earlier. This strict timeline ensures the RBI has updated records of foreign ownership in your Private Limited company. Missing this window triggers mandatory late fees and administrative delays.

Who is responsible for filing the FC-TRS form, the buyer or the seller?

The responsibility for filing the FC-TRS form lies with the resident party involved in the transaction. If a resident Indian sells shares to a non-resident, the resident seller must file the form. Conversely, if a resident buys shares from a non-resident, the resident buyer takes on the reporting duty through their AD bank.

Can I file FC-TRS without a Valuation Certificate?

You cannot file Form FC-TRS without a valid Valuation Certificate from a Chartered Accountant or a SEBI-registered merchant banker. The RBI requires this document to ensure the transaction meets the Fair Market Value (FMV) guidelines. This certificate proves that the shares weren’t sold below the floor price or bought above the cap price.

What happens if I miss the 60-day deadline for FCTRS filing?

Missing the 60-day deadline results in a mandatory Late Submission Fee (LSF) to regularize the delay. Beyond the financial cost, chronic delays can lead to increased scrutiny from the Enforcement Directorate (ED). It may also block your ability to repatriate funds or exit the business until the RBI clears the contravention.

Is FCTRS filing required for a gift of shares to a non-resident?

Yes, FCTRS filing is mandatory if a resident individual gives shares as a gift to a non-resident. This process often requires prior approval from the RBI if the value of the gift exceeds specific regulatory limits. You must report the transfer on the FIRMS portal to maintain an accurate and transparent foreign investment record.

What is the Late Submission Fee (LSF) for FC-TRS?

The LSF is calculated using the formula: ₹7,500 + (0.025% × A × n). In this equation, ‘A’ represents the transaction amount and ‘n’ is the number of years of delay, rounded up to the nearest month. The total fee is capped at 100% of the amount involved in the transfer, as per RBI Circular No. 16 dated September 30, 2022.

Do I need to file FC-TRS for a transfer between two non-residents?

Reporting is generally not required for transfers between two non-residents unless the Indian company is directly involved in the remittance of funds. However, the company must still update its records in the next Annual Return on Foreign Liabilities and Assets (FLA). You should always verify specific sector requirements with your AD bank to ensure total compliance.

How long does the AD bank take to approve an FCTRS filing?

Most Authorized Dealer (AD) banks take between 15 to 30 business days to approve a filing. This timeline depends on the accuracy of your documentation and the clarity of your valuation report. If the bank finds discrepancies in your KYC or FIRC details, they’ll return the form for clarification, which extends the total processing time.

Article by

Nihal Srivastava

Nihal Srivastava is the Co-Founder of Krystal7 Consultants, helping Indian entrepreneurs and startups navigate company registration, compliance, trademark protection, and regulatory requirements with clarity and confidence. With 6+ years of hands-on expertise in MCA filings, GST compliance, and corporate structuring, Nihal has guided 1000+ businesses across India through their legal and compliance journeys. He believes every business dream deserves crystal clear foundations, and that no founder should be held back by paperwork or red tape.