Transfer Pricing Study in India: A 2026 Compliance Guide for Foreign Subsidiaries

In 2026, a transfer pricing study in India is no longer just a tedious checkbox for your compliance team; it’s a strategic shield that protects your subsidiary’s global profits from aggressive tax audits. You likely feel the weight of the new Income-tax Act 2025 and the anxiety that comes with shifting regulations. We understand that managing cross-border transactions can feel like walking a tightrope while the rules of the game are being rewritten.

This guide empowers you to master these complexities, ensuring your operations remain transparent and audit-proof under the 2026 tax law reset. You’ll gain a clear understanding of the updated Arm’s Length Principle and how to protect your business from the high costs of specialized tax consulting. We’ll also provide a practical roadmap for your documentation requirements to help you avoid the stress of tax litigation.

We’ve included a vital checklist of 2026 deadlines, including the October 31 cutoff for the new Form 48 and the November 30 deadline for your Income Tax Return. Our methodical approach brings order to these complicated processes, granting you the operational liberty to focus on your core business goals. By the end of this article, you’ll have the tools to navigate the tax portals with calm competence and total precision.

Key Takeaways

- Understand how the new Income-tax Act, 2025 reshapes compliance for foreign subsidiaries and why a proactive strategy is essential for the 2026 tax year.

- Master the Arm’s Length Principle to ensure your international transactions are priced fairly, supported by a comprehensive transfer pricing study India mandates for transparency.

- Navigate the mandatory three-tier documentation structure, including the Local File and Master File, to keep your records audit-ready and compliant.

- Explore how Safe Harbor rules and Advance Pricing Agreements can provide long-term tax certainty and protect your business from aggressive litigation.

- Learn to identify and value intercompany deals methodically, turning complex bureaucratic obstacles into a strategic advantage for your company’s growth.

Understanding Transfer Pricing in India: Why Your Business Needs a Study in 2026

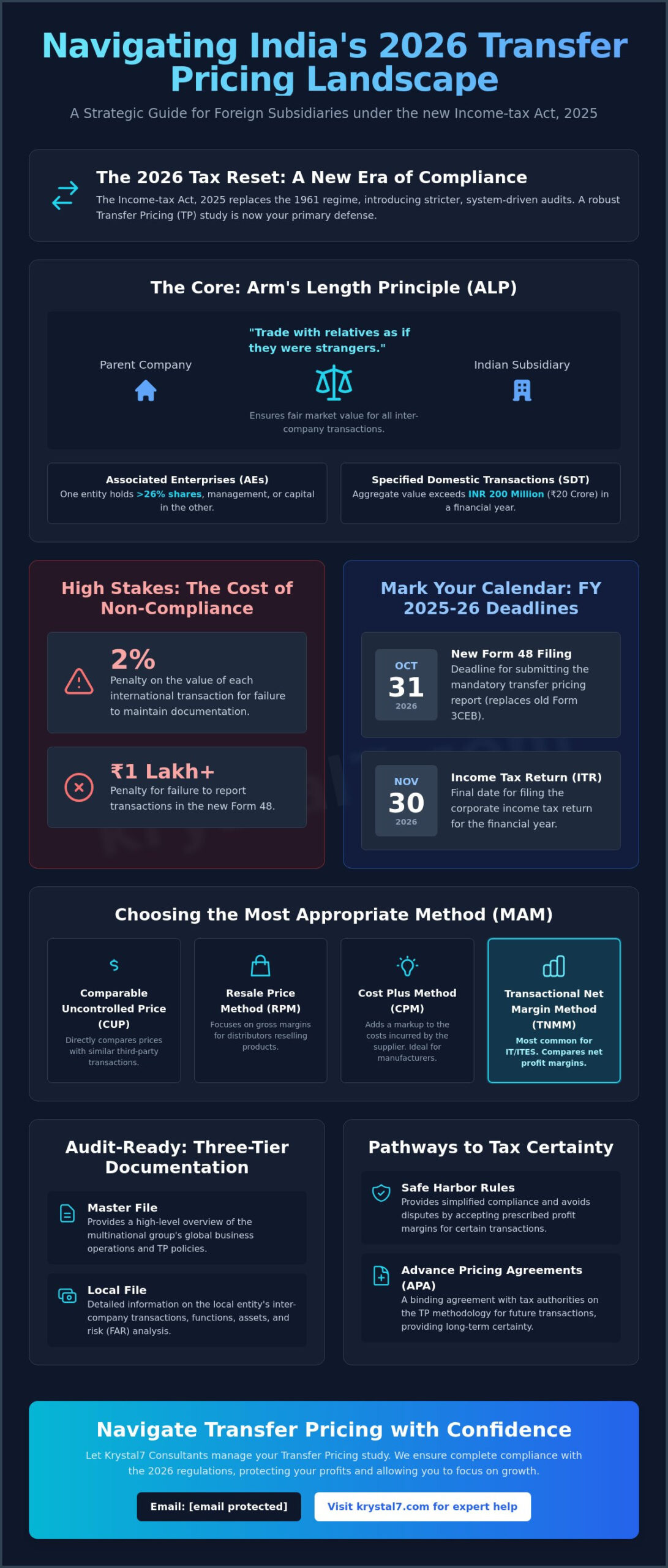

The regulatory landscape for foreign subsidiaries in India shifted on April 1, 2026. The introduction of the Income-tax Act 2025 and the Income-tax Rules 2026 marked the end of the decades-old 1961 regime. This major reset means that a transfer pricing study India mandates is no longer just a routine annual filing; it’s your primary defense against aggressive tax audits and heavy penalties.

At its core, Transfer pricing refers to the pricing of transactions between Associated Enterprises (AEs). Under Section 92A of the Act, companies are considered AEs if one participates in the management, control, or capital of the other. For example, if a parent company in the US owns more than 26% of the shares in an Indian Private Limited company, they’re classified as AEs. These regulations also cover Specified Domestic Transactions when the aggregate value exceeds INR 200 million (20 Crore) within a single financial year.

The Core Architecture: Income-tax Act 2025 and 2026 Rules

The 2026 reset aims to provide a more predictable and transparent tax environment for visionaries looking to expand in India. The Central Board of Direct Taxes (CBDT) has updated the standards to align with international best practices, specifically targeting “tax base erosion.” Foreign subsidiaries are the primary focus because the government wants to ensure that profits stay where the actual value is created. By maintaining a robust transfer pricing study India requires, you show the tax department that your intercompany deals are handled with visual precision and honesty. This shift toward a system-driven approach means that your internal records must match your external filings with absolute clarity.

The Risk of Non-Compliance: Penalties and Audits

The cost of ignoring these rules is high. If your business fails to keep the mandatory documentation, the penalty is a steep 2% of the value of each international transaction. Additionally, failing to report these deals in the new Form 48, which replaces the old Form 3CEB, results in a penalty starting at INR 1 Lakh. The 2026 focus is on reducing litigation through better upfront documentation. The tax department now uses automated, rule-based systems to flag inconsistencies. A methodical study helps you avoid the administrative burden of lengthy disputes. It provides the security you need to focus on growth while we handle the complexity of the Indian tax portal.

The Arm’s Length Principle: How India Determines Fair Market Value

Imagine your Indian Private Limited subsidiary provides software services to its parent company in London. The tax department wants to ensure you aren’t undercharging just because you’re “family.” This is where the Arm’s Length Principle (ALP) comes in. It simply means trading with relatives as if they were strangers. To prove this, a meticulous transfer pricing study India requires you to find similar deals between unrelated companies.

You must select the “Most Appropriate Method” (MAM) to calculate this fair value. The Income-tax Rules 2026 don’t allow for guesswork. They require a logical selection based on the nature of your transaction and the availability of data.

The Five Standard TP Methods in India

- Comparable Uncontrolled Price (CUP) Method: This directly compares the price of your goods or services to what a stranger would pay in a similar setting.

- Resale Price Method (RPM) and Cost Plus Method (CPM): These focus on gross margins. RPM is usually for distributors, while CPM works well for manufacturers.

- Transactional Net Margin Method (TNMM): This is the most common choice for Indian IT and ITES subsidiaries. It compares net profit margins rather than individual prices.

Benchmarking Analysis and Economic Justification

To find these “stranger” companies, we use specialized Indian databases like Prowess or Capitaline. We look for companies with similar functions, assets, and risks. This is known as a FAR analysis. It’s the backbone of your transfer pricing study India compliance. It details exactly what your Indian team does, the equipment they use, and the risks they take on.

The range concept is a statistical tool where the tax department accepts your price if it falls between the 35th and 65th percentile of the comparable prices found in the market. This provides a safety net for your business. It allows for minor market fluctuations without triggering an immediate audit.

Our team at Krystal7 helps you identify the best benchmarking strategy to ensure your cross border compliances are handled with visual transparency. We bring order to these complicated processes so you can focus on your primary business goals.

Documentation Requirements: The Three-Tier Structure in 2026

India’s tax framework for 2026 follows a strict three-tier documentation structure. This system ensures that every level of your multinational group remains transparent to the tax authorities. The first tier is the Local File. This is the actual transfer pricing study India mandates for every taxpayer with international transactions. For larger multinational groups, the second tier is the Master File, filed using Form 3CEAA. It provides a high-level overview of global operations and intellectual property. The third tier is Country-by-Country Reporting (CbCR) in Form 3CEAD. This applies to ultra-large entities with consolidated group revenues exceeding specific global thresholds.

The Local File: Your Annual Transfer Pricing Study

The Local File acts as the heart of your compliance strategy. It includes a deep industry analysis, a detailed entity profile, and a breakdown of every intercompany transaction. You must update this study annually even if your business model hasn’t changed. Market conditions, interest rates, and comparable profit margins fluctuate every year. This makes fresh benchmarking essential for your security. This document is a critical part of your annual compliance for private limited company obligations. Keeping it updated ensures that your filings reflect the current economic reality of the Indian market.

Form 3CEB: The Chartered Accountant’s Certification

While the study is your internal defense, Form 3CEB is the official summary filed on the tax portal. Under the 2026 rules, this report is being replaced by Form 48. This document must be certified by a Chartered Accountant and submitted by October 31, 2026. This certification confirms that your international transactions adhere to the Arm’s Length Principle. Consistency is vital here. The data in your internal transfer pricing study India must match the figures reported in your income tax return. The deadline for filing the tax return and the Master File is November 30, 2026. Discrepancies between these documents are the most common triggers for a detailed tax audit. We provide the methodical oversight needed to ensure every number aligns perfectly. This gives you the security to grow without administrative anxiety.

Safe Harbor Rules vs. Advance Pricing Agreements (APA)

Choosing the right compliance path is a major decision for any foreign subsidiary in 2026. The major reset of the Income-tax Rules 2026 has overhauled both Safe Harbor provisions and Advance Pricing Agreements (APAs). While a transfer pricing study India usually involves detailed benchmarking, these two options offer alternative routes to manage your tax risk. One prioritizes simplicity, while the other offers long-term peace of mind.

Opting for Safe Harbor in 2026

Safe Harbor provisions act as a “no-questions-asked” agreement with the Income Tax Department. If your Indian subsidiary reports a profit margin equal to or higher than the prescribed rate, the tax office won’t challenge your pricing. For the 2026-27 Assessment Year, the government has set a uniform safe harbor margin of 15.5% on cost for IT services. This category now includes software development, IT-enabled services, and KPO services. The eligibility threshold for this regime has also seen a massive increase, rising from INR 3 billion to INR 20 billion in turnover.

The primary benefit of this route is the complete avoidance of a transfer pricing audit. It eliminates the administrative burden of defending your margins in court. However, there’s a catch. The 15.5% margin might be significantly higher than what you’d find in a standard transfer pricing study India benchmarking analysis. You’re essentially paying a premium in taxes in exchange for absolute procedural simplicity. This is often the best fit for smaller startups or subsidiaries with straightforward service models.

Advance Pricing Agreements (APA): Long-Term Peace of Mind

Advance Pricing Agreements (APA) represent the gold standard of tax certainty. An APA is a proactive deal negotiated with the Central Board of Direct Taxes (CBDT) that fixes your pricing methodology for up to nine years. This includes five future years and four “rollback” years. Under the 2026 rules, the application process is more streamlined. A flat fee of INR 20 lakh applies to all APA applications, and unilateral APAs for the IT sector are being fast-tracked with a two-year completion target.

Established MNCs with complex, high-value transactions typically prefer this route. It provides total immunity from future litigation and allows associated enterprises to file modified tax returns to claim refunds if needed. While the upfront cost and negotiation time are higher than Safe Harbor, the long-term savings and security are unmatched. If you’re unsure which path aligns with your growth strategy, our team can help you evaluate your annual compliance package options to find the most cost-effective solution.

Conducting Your Transfer Pricing Study with Krystal7 Consultants

Managing a global business requires a clear focus on vision and growth. However, the administrative weight of Indian tax laws can often feel like a bureaucratic obstacle. At Krystal7, we remove this burden by providing a methodical transfer pricing study India mandates for foreign subsidiaries. Our approach ensures that your intercompany transactions are valued with visual transparency, protecting you from the risk of heavy penalties.

Compliance begins long before the audit season. It starts with your foreign subsidiary registration. We integrate transfer pricing planning into your initial setup to ensure your profit margins align with the Arm’s Length Principle from day one. This proactive strategy grants you the operational liberty to scale your business without fear of future litigation.

Our Step-by-Step Compliance Process

We bring order to complicated processes through a structured three-step approach. This methodical path ensures that every detail of your business is documented for the tax authorities.

- Step 1: Transaction Identification and FAR Analysis. We map every deal between your Indian unit and its global parent. We conduct a detailed Functions, Assets, and Risks (FAR) analysis to define the economic reality of your operations.

- Step 2: Database Benchmarking and ALP Computation. Our experts use elite Indian databases like Prowess to find comparable market prices. We then compute the Arm’s Length Price (ALP) to justify your intercompany margins.

- Step 3: Preparation of the Study and Filing. We draft the comprehensive transfer pricing study India requires and prepare the Accountant’s Report. Under the 2026 rules, we ensure your Form 48 is filed accurately by the October 31 deadline.

Why Gurgaon Startups Trust Krystal7 for Tax Advisory

Gurgaon is the heart of India’s startup ecosystem. Our team understands the specific regulatory environment of Haryana and the unique needs of tech-driven founders. We believe in financial openness, which is why we offer clear, fixed-fee pricing models with no hidden costs. This commitment to transparency builds a foundation of reliability for our long-term partners.

Delegating your tax compliance to us is an investment in your company’s future success. Our “Liberation Theme” is simple: we handle the complexity so you can pursue your primary goals. Contact our elite consultants today for a meticulous review of your cross-border transactions. Reach out to us at business@krystal7.com or visit krystal7.com to secure your business for 2026 and beyond.

Secure Your Subsidiary’s Success in the 2026 Tax Era

The 2026 tax reset introduces a new era of transparency and precision for foreign subsidiaries. By mastering the Arm’s Length Principle and selecting the right compliance path, you turn a bureaucratic hurdle into a strategic advantage. Whether you opt for the simplicity of Safe Harbor or the long-term certainty of an APA, your documentation must be meticulous. A robust transfer pricing study India requires is your best defense against audits and heavy penalties.

At Krystal7 Consultants, our Chartered Accountant led team specializes in foreign subsidiary compliance. We bring order to these complex regulations with transparent pricing models designed for startups and SMEs. We’ll handle the administrative complexity so you can focus on your primary business goals. It’s time to gain operational liberty and protect your cross-border transactions with confidence.

Contact Krystal7 Consultants for a Transfer Pricing Study at business@krystal7.com or visit krystal7.com for expert assistance. Your journey as a visionary entrepreneur deserves a partner who values your growth as much as you do.

Frequently Asked Questions

Is a transfer pricing study mandatory for every Indian company?

A transfer pricing study India requires is only mandatory if your business enters into international transactions with Associated Enterprises (AEs). It also applies to Specified Domestic Transactions if the total value exceeds INR 200 million in a single financial year. If your Private Limited company only deals with unrelated local vendors, you don’t need this specific documentation.

What is the deadline for filing the transfer pricing report in 2026?

The deadline for filing the Accountant’s Report for the Financial Year 2025-26 is October 31, 2026. This report, traditionally known as Form 3CEB, is being transitioned to Form 48 under the new Income-tax Rules 2026. Missing this deadline triggers a graded fee structure where the penalty increases based on the length of the delay.

Can I use a global transfer pricing study for my Indian subsidiary?

You cannot simply use a global master file to satisfy Indian requirements. While global documentation provides a helpful overview, the Indian tax department demands a localized study using Indian databases like Prowess or Capitaline. Your local file must reflect the specific economic conditions and profit margins found within the Indian market to be considered valid.

What happens if the tax department rejects my arm’s length price?

If the tax department rejects your arm’s length price, they will recompute the transaction value using their own benchmarking data. This usually results in a higher taxable income for your subsidiary and an immediate tax demand. You’ll also face a penalty of 2% of the transaction value for failure to maintain proper documentation.

Are domestic transactions between two Indian companies subject to transfer pricing?

Yes, domestic transactions are subject to these rules if they qualify as Specified Domestic Transactions. This typically happens between two related Indian entities where one enjoys a tax holiday or specific tax deductions. The regulations trigger once the aggregate value of these transactions crosses the INR 200 million threshold in a year.

What is the “range concept” in Indian transfer pricing rules?

The range concept is a statistical method used to validate your pricing against market data. Your price is considered at arm’s length if it falls between the 35th and 65th percentile of the prices charged by comparable companies. This provides a necessary buffer for minor price variations and reduces the likelihood of an immediate tax dispute.

How much does a transfer pricing study typically cost for an SME?

The cost of a transfer pricing study India mandates varies based on the volume and complexity of your intercompany transactions. Professional fees for a Chartered Accountant led firm depend on the number of international deals and the depth of benchmarking required. You should request a transparent, fixed-fee quote to ensure your compliance budget remains predictable and clear.

How long is a transfer pricing study valid in India?

A transfer pricing study is valid for only one financial year in India. You must update your benchmarking and documentation annually to reflect changing market conditions and new financial data. Even if your intercompany agreements stay the same, the profit margins of comparable companies in the database will fluctuate every year, making fresh analysis essential.

Article by

Nihal Srivastava

Nihal Srivastava is the Co-Founder of Krystal7 Consultants, helping Indian entrepreneurs and startups navigate company registration, compliance, trademark protection, and regulatory requirements with clarity and confidence. With 6+ years of hands-on expertise in MCA filings, GST compliance, and corporate structuring, Nihal has guided 1000+ businesses across India through their legal and compliance journeys. He believes every business dream deserves crystal clear foundations, and that no founder should be held back by paperwork or red tape.